Who is the VAT tax agent? Who is recognized as a tax agent for VAT (responsibilities, nuances) Postings for VAT tax agent in foreign currency

VAT of the tax agent is taken into account if:

the purchase of goods is carried out in foreign currency from a non-resident;

the property is leased;

the property is for sale.

To account for VAT, accounts 76.NA and 68.32 are used. We propose to analyze all three situations and determine the specific features of the invoice design.

The main condition when purchasing goods in foreign currency from a non-resident is to correctly fill out the contract parameters:

Type of contract – indicate “With supplier”;

The organization acts as a tax agent for the payment of VAT – check the box;

Type of agency agreement – indicate “Non-resident”.

We process the receipt of goods in the standard way, but without registering an invoice:

In the movement of the document, the subaccount 76.NA will be used, and not the usual settlement account.

To reflect VAT, special processing will be used, which can be found on the menu tab “Bank and cash desk” section “Registration of invoices” journal “Tax agent invoices”:

Open the form. You only need to specify the period and name of the agent organization (if the 1C program is used to maintain accounting for several companies at the same time, for example, when using 1C online remotely). Filling out is automatic by clicking “Fill”, and all the necessary documents will be displayed in the tabular section.

By clicking “Run”, invoices will be generated and registered:

In the invoice form, pay attention to the indicated VAT rate - “18/118” and the designation of the transaction code - 06.

The postings will reflect special accounts 76.NA and 68.32, which are added to the chart of accounts:

The amount of VAT for mandatory payment to the budget is checked through the “Sales Book” report and through the “VAT Declarations” document. The “Sales Book” report is generated in the “VAT Reports” section.

In this case, the period of formation and the name of the tax payer organization are indicated:

The VAT return is generated in the “Reporting” section, “Regulated reports”, “VAT return”. The value of the amount for payment will be reflected on page 1 section 2 in line 060:

The tax is paid through standard documents of the 1C program “Payment order” and “Write-off from the current account”, in which the “Type of transaction” - “Payment of tax” must be indicated.

Please note that in order to correctly write off VAT, you must indicate account 68.32.

After this we accept VAT for deduction. Go to the menu tab “Operations” section “Routine VAT operations”.

Create a document “Creating Purchase Book Entries” and open the “Tax Agent” tab:

We post the document and look at the movement in the document “Creating purchase ledger entries”:

Then we move on to creating the “Purchase Book” document, which is located in the “VAT Reports” section. The column “Name of the seller” will appear not as the agent organization, but as the seller organization:

If you look at the declaration, then on page 1 section 3 of term 180 you can see the value of the amount for deduction for the tax agent operation:

The sale of property through a tax agent is formalized indicating the correct type of agreement and in compliance with the fixed asset accounting regulations:

Below is the sequence of registration of invoices by a tax agent:

creation of an agency agreement;

posting of goods or services under the specified agreement;

payment for goods or services to the supplier

registration of tax agent invoice;

payment of VAT to the budget;

acceptance of VAT for deduction through the document “Creating purchase ledger entries.”

Elena Potemina, Deputy Head of Department

tax and financial consulting "Intercom-Audit"

Organizations seeking to conscientiously and fully fulfill the duties of a tax agent are faced with a large number of ambiguities and contradictions in the established procedure for calculating and paying VAT. Despite the constant changes made to the Tax Code of the Russian Federation, some issues remain unresolved. This article discusses the procedures for paying VAT to the budget by a tax agent, as well as applying the deduction. The article highlights changes in tax legislation introduced by Federal Law No. 224-FZ of November 26, 2008, regarding the duties of tax agents for VAT: whether these changes reduce existing tax risks or lead to the emergence of new ones.

The concept of “tax agent” is disclosed in paragraph 1 of Article 24 of the Tax Code of the Russian Federation:

« Tax agents are persons who, in accordance with this Code, are entrusted with the duties of calculating, withholding from the taxpayer and transferring taxes to the budget system of the Russian Federation».

Cases when an organization or individual entrepreneur is recognized as tax agents for VAT are established in Article 161 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation).

Table 1. Cases in which the duty of a tax agent for VAT arises

Key moment |

Legal relations |

Object/Participant |

Tax agent |

Norm of the Tax Code of the Russian Federation |

Validity period of the norm |

|

Purchase of goods (works, services) |

Goods (work, services), the place of sale of which is recognized as the Russian Federation |

Buyer (customer) registered with the Russian tax authorities |

||||

A foreign person not registered with the tax authorities |

Mediation (assignment, commission, agency) with participation in settlements during sales in the Russian Federation |

Goods, transfer of property rights, performance of work, provision of services on the territory of the Russian Federation |

Intermediary involved in settlements based on agency agreements, commission agreements or agency agreements |

*01.01.2009 |

||

Federal or municipal property, property of constituent entities of the Russian Federation |

Obtaining a lease on the territory of the Russian Federation |

Bodies of state power and administration and local governments |

Tenant |

|||

State or municipal property not assigned to state or municipal enterprises and institutions |

Purchase (receipt) in the Russian Federation |

Buyer (recipient) of property |

||||

Confiscated property, property, implemented by court decision *, ownerless values, treasures and purchased values, as well as values transferred by right of inheritance to the state |

Sales in the Russian Federation |

Body, organization or individual entrepreneur selling such property |

* 01.01.2009 |

|||

The organization is a ship owner |

Carrying out operations specified in clause 6 of Art. 161 Tax Code of the Russian Federation. |

Owner of the vessel on the date of operation |

In practice, the duties of a tax agent often arise for two reasons - the acquisition of goods, works, services from a foreign person who is not registered with the tax authorities of the Russian Federation, and the lease of federal property, property of constituent entities of the Russian Federation and municipal property. Moreover, it is precisely these groups of tax agents that raise a large number of questions.

According to paragraph 1 of Art. 161 of the Tax Code of the Russian Federation, when selling goods (work, services), the place of sale of which is the territory of the Russian Federation, by taxpayers - foreign persons who are not registered with the tax authorities as taxpayers, the tax base is determined as the amount of income from the sale of these goods (work, services) including tax. Please note that not every purchase from a foreign counterparty gives rise to the obligation of a tax agent. First of all, the operation being carried out must be subject to value added tax. The answer to the question whether Russia is a place of sale of goods, works, and services is contained in the norms of Articles 147 “Place of sale of goods” and 148 “Place of sale of works (services)” of the Tax Code of the Russian Federation. The second circumstance indicating the emergence of the duty of a tax agent is the fact that the foreign seller is not registered with the tax authorities of the Russian Federation.

Let us dwell in detail on such a moment as the recalculation of agent VAT into rubles. After all, it is in this currency that taxes must be paid to the Russian budget (Clause 5, Article 45 of the Tax Code of the Russian Federation).

The tax amount is calculated by the tax agent separately for each transaction involving the sale of goods (work, services) on the territory of the Russian Federation based on the tax base (clauses 1 and 3 of Article 166 of the Tax Code of the Russian Federation). In this case, the “total amount of tax” is not calculated, and accordingly, there is no reason to apply the provisions of paragraph 4 of Article 166 of the Tax Code of the Russian Federation, which ties the date of tax calculation to the moment the tax base is determined. Based on the wording of paragraph 3 of Article 166 of the Tax Code of the Russian Federation “ the tax amount is calculated...separately for each sales transaction", we can say that the tax must be calculated in this case precisely at the moment of transfer of ownership of goods, results of work, provision of services to the tax agent (clause 1 of Article 39 of the Tax Code of the Russian Federation).

To calculate tax, you need to determine the total value of the tax base. The general principles for determining the tax base for VAT are established by Article 153 of the Tax Code of the Russian Federation. Paragraph 1 reads: " The tax base for the sale of goods (work, services) is determined by the taxpayer in accordance with this chapter, depending on the specifics of the sale of goods (work, services) produced by him or purchased externally." This means that in addition to the general procedure for calculating the tax base, special rules may be provided for individual cases.

So, for the case of the sale of goods (work, services), the place of sale of which is the territory of the Russian Federation, by taxpayers - foreign persons who are not registered with the tax authorities as taxpayers, paragraph 1 of Article 161 of the Tax Code of the Russian Federation establishes the following features:

The tax base is calculated by tax agents;

The tax base in this case is the amount of income from the sale of goods (work, services) including VAT;

The tax base is determined separately for each transaction involving the sale of goods (works, services), and not as a whole based on the results of the tax period.

Chapter 21 of the Tax Code of the Russian Federation does not establish other features of calculating the tax base for transactions involving the sale of goods (works, services) by foreign organizations. In particular, the Tax Code does not formally establish a special point in determining the tax base of the Tax Code of the Russian Federation.

Typically, Russian taxpayers make settlements with foreign companies in foreign currency. According to paragraph 3 of Article 153 of the Tax Code of the Russian Federation “ when determining the tax base, the taxpayer's proceeds (expenses) in foreign currency are recalculated into rubles at the rate of the Central Bank of the Russian Federation, respectively, on the date corresponding to the moment of determining the tax base for the sale (transfer) of goods (work, services), property rights, established by Article 167 of this Code, or on the date of actual expenses».

The moment of determining the tax base is the earliest of the following dates (clause 1 of Article 167 of the Tax Code of the Russian Federation):

1) the day of shipment (transfer) of goods (work, services), property rights;

2) the day of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights.

It turns out that when paying income to a foreign taxpayer in the form of advance payments for goods (work, services) purchased from him, the tax agent must use the date of transfer of funds as such a date; accordingly, tax is transferred to the budget at this rate. Based on the provisions of paragraph 14 of Article 167 of the Tax Code of the Russian Federation, in the future, when receiving goods (work, services) from a foreign person on account of this advance, the amount of its proceeds must be recalculated at the rate already on the date of shipment.

If, however, goods (works, services) are received from a foreign company first, that is, the moment comes to determine the tax base in accordance with subparagraph 1 of paragraph 1 of Article 167 of the Tax Code of the Russian Federation, and only then they are paid for, the date of recalculation is taken on the day of shipment (transfer) of goods (works) , services) and remains unchanged.

The difficulty is that the opportunity to withhold tax from amounts due to a foreign organization exists only at the time of transfer, including advance payments. And as stated above, it is not possible to calculate the amount of tax in full compliance with the norms of Chapter 21 of the Tax Code of the Russian Federation at the time of payment of the advance.

The practice of applying the provisions of Chapter 21 of the Tax Code of the Russian Federation in the case provided for in paragraph 1 of Article 161 developed completely differently from its formal reading set out above.

In the previously existing Methodological Recommendations for the application of Chapter 21 “Value Added Tax” of the Tax Code of the Russian Federation, approved by Order of the Ministry of Taxes and Taxes of Russia dated December 20, 2000 N BG-3-03/447, paragraph 32.2 directly stated that in the case provided for in paragraph 1 of Article 161 Tax Code of the Russian Federation, the tax base for the sale of goods (work, services) for foreign currency, determined by the tax agent, is calculated by recalculating the tax agent's expenses in foreign currency into rubles at the exchange rate of the Central Bank of the Russian Federation on the date of sale of goods (work, services), that is, on the date transfer of funds by a tax agent in payment for goods (work, services) to a foreign person who is not registered with the tax authorities as a taxpayer. The tax agent recalculates the tax base when selling goods (work, services) for foreign currency into rubles at the rate of the Central Bank of the Russian Federation on the date of actual expenses (including if these expenses are advance or other payments), regardless of the adopted accounting policy for tax purposes.

Clause 32.2 By Order of the Ministry of Taxes of Russia dated September 19, 2003 N BG-3-03/499, clause 32.2 was excluded from the text of the Methodological Recommendations on VAT, and currently the Methodological Recommendations have lost force (Order of the Federal Tax Service of Russia dated 12.12.2005 N SAE- 3-03/665@), but in practice the approach set out there continues to be used by tax authorities. The position of the tax department on this issue was confirmed by Letter of the Ministry of Taxes of Russia dated September 24, 2003 N OS-6-03/995@ “On the procedure for calculating and paying value added tax.” Despite the age of this letter, most expert consultations contain a reference to this document as a substantiation of the consultant’s position. The conclusions presented in the letter do not stand up to any criticism, moreover, they are not based on the provisions of the Tax Code, however, this letter at least to some extent reduces the existing uncertainty on this issue. Moreover, the stated position of the tax authorities is convenient for organizations that are tax agents, in the light of the application of the right to deduct VAT withheld and paid to the budget.

A similar position is contained in Letter of the Ministry of Finance of Russia dated July 3, 2007 N 03-07-08/170, regarding the application of a deduction for VAT amounts withheld by a Russian organization as a tax agent. According to financial department specialists, the Russian taxpayer calculates the VAT tax base by converting it into rubles at the Bank of Russia exchange rate. on the date of actual expenses", and it is this amount that he has the right to accept as a deduction, without recalculating it on the date of registration of goods, works and services. The taxpayer’s question was what amount was deductible: “ determined and paid on the date of payment of income to a foreign person (clause 4 of Article 174 of the Tax Code) or determined on the date of registration of the service (clause 1 of Article 172 of the Tax Code)" Based on the answer, it turns out that specialists from the Ministry of Finance are also of the opinion that in order to determine the tax base for VAT, the date of the expense is the date of payment to the foreign organization for goods, work, and services.

Thus, the approach of tax and financial authorities is based on the recognition of the fact that in the case of withholding VAT from the income of a foreign organization by a tax agent, there is a special moment for determining the tax base - based on the date of payment to the foreign counterparty.

Taking into account the fact that the norms of Chapter 21 of the Tax Code of the Russian Federation do not allow defining a clear algorithm for calculating the amount of tax to be withheld from the income of a foreign organization, but at the time of transferring the advance to the Russian side it is necessary to fulfill the requirement of tax legislation and withhold VAT, we consider it possible to use the approach recommended for calculation in the explanations of the tax authorities.

That is, on the date of making a payment to a foreign counterparty, the Russian organization calculates the amount of tax based on the ruble estimate of the revenue of the taxpayer - a foreign organization, recalculated at the exchange rate on the date of payment. Consequently, the amount of tax calculated for payment to the budget by the tax agent has been determined. The fact of tax withholding from amounts due to a foreign counterparty and the occurrence of a tax agent’s obligation to the budget is reflected by the organization with the following entry in the accounting accounts: debit of account 60 “Settlements with suppliers and contractors” and credit of account.

Now let’s consider the emergence of obligations for the second “popular” group of tax agents. These are tenants of federal property, property of constituent entities of the Russian Federation and municipal property.

Please pay attention to the following point, paragraph 3 of Article 161 of the Tax Code of the Russian Federation indicates that the obligation of a tax agent arises only for those persons who rent property directly from state authorities and management bodies or local governments. On behalf of these bodies, as a rule, state property management committees (SPMC) (property departments) act.

Civil legislation establishes that under a lease (property lease) agreement, the lessor (lessor) undertakes to provide the lessee (tenant) with property for a fee for temporary possession and use or for temporary use. That is, legal relations arise between two persons. In practice, three-party lease agreements for state or municipal real estate with the participation of budgetary institutions are used. The institution is named in these agreements as a balance holder , and public authorities (local governments) - in the role of lessor . The question arises whether this construction of the agreement changes the circumstances of the occurrence of the tax agent’s obligation.

When the lessor of state property is directly an organization to which such property belongs under the right of economic management or operational management, the lessee of this property, in accordance with the letter of the law, should not perform the duties of a tax agent for VAT. Landlord organizations calculate and pay VAT to the budget independently. This position was expressed in the Ruling of the Constitutional Court of the Russian Federation dated October 2, 2003 N 384-O. The court indicated that the procedure for paying tax established by paragraph 3 of Art. 161 of the Tax Code of the Russian Federation, applies in the case of leasing public property that is not assigned the right of economic management or operational management to a federal state unitary enterprise, that is, constituting the state treasury (paragraph 2, paragraph 4, article 214 of the Civil Code of the Russian Federation), with the direct participation of public owners in civil legal relations. It turns out that if the lessor is a balance holder, for example a government company, then clause 3 of Art. 161 of the Tax Code of the Russian Federation does not apply. The taxpayer in this case is an individual who is capable of independently paying the tax in the generally established manner.

An analysis of arbitration practice on the issue of the legality of holding an organization-tenant of state property liable for failure to fulfill the duties of a tax agent shows that the courts in most cases proceed from their actual content of the relationship, first of all, paying attention to whether it was ultimately paid to the budget VAT. For example, in the Resolution of the Federal Antimonopoly Service of the Moscow District dated September 28, 2006 N KA-A40/7292-06, the arbitrators refused to collect VAT and penalties for non-payment of tax from the tenant-agent, since the lease agreement stated that the tenant transfers the entire amount of the rent to the balance holder , including VAT, and the latter pays VAT to the budget. When a tripartite agreement contains an indication that the tenant transfers VAT to the budget, but in fact does not do this, the court recognizes the tax accrual to him as lawful (Resolution of the Federal Antimonopoly Service of the Volga District dated November 4, 2006 N A65-41609/05-SA1-32).

It should be noted that the absence in the lease agreement of a condition on the tenant’s obligation to withhold VAT from the lessor’s income and transfer to the budget is not provided for by tax legislation as a basis for exempting the tax agent from fulfilling the duties established in paragraph 3 of Art. 161 of the Tax Code of the Russian Federation (Resolution of the Federal Antimonopoly Service of the West Siberian District dated September 24, 2007 N F04-6501/2007 (38740-A27-42).

Thus, the tenant does not face claims from the tax authorities regarding the performance of the duties of a tax agent only in the case when he receives property for rent under a bilateral agreement directly with the balance holder

Cases of application of estimated rates for calculating the amount of VAT are indicated in paragraph 4 of Art. 164 of the Tax Code of the Russian Federation, including this applies to the withholding of tax by tax agents in accordance with paragraphs 1 - 3 of Art. 161 Tax Code of the Russian Federation. The tax base is determined taking into account the tax. When fulfilling the duty of a tax agent on the basis of paragraphs 4-6 of Article 161 of the Tax Code of the Russian Federation, the tax base is determined based on the sales price excluding the amount of VAT. Therefore, tax must be calculated at a direct rate.

Until recently, the question remained debatable whether organizations that are tax agents on the basis of paragraphs 2 and 3 of Article 161 of the Tax Code of the Russian Federation are required to issue an invoice. The changes made to Article 168 of the Tax Code of the Russian Federation by Federal Law No. 224-FZ of November 26, 2008 are intended to bring certainty.

Clause 3 of Article 168 of the Tax Code of the Russian Federation has been supplemented with a second paragraph: “ When calculating the amount of tax in accordance with paragraphs 1 - 3 of Article 161 of this Code, tax agents specified in paragraphs 2 and 3 of Article 161 of this Code draw up invoices in the manner established by paragraphs 5 and 6 of Article 169 of this Code».

According to the author, this new provision cannot be considered as a requirement to issue an invoice in the same manner as taxpayers, but only determines the content of the document drawn up by the tax agent. Clauses 5 and 6 of Article 169 of the Tax Code of the Russian Federation establish a list of mandatory details for an invoice issued for the sale of goods (work, services). The instruction to draw up an invoice “when calculating the amount of tax” can be interpreted as a reference to the moment of determining the amount of tax to be paid to the budget by the tax agent. In the cases under consideration, the tax agent cannot “present” the tax to the buyer, since he himself is the buyer. Therefore, neither upon sale nor upon receipt of payment, the tax agent is not required to draw up an invoice. The tax agent calculates the amount of tax for each transaction for the sale of goods, works, services, and as a result of such calculation an invoice is issued.

It is impossible to unambiguously assess how this addition to Article 168 of the Tax Code of the Russian Federation will affect the procedure for applying the VAT deduction paid by the tax agent. However

Tax agents, as well as taxpayers, present the results of the tax period (quarter) declaration to the tax authorities at the place of your registration. The general deadline for submitting the declaration is no later than the 20th day of the month following the expired tax period (clause 5 of Article 174 of the Tax Code of the Russian Federation). Persons acting as tax agents fill out section 2 of the declaration form approved by Order of the Ministry of Finance of Russia dated November 7, 2006 N 136n. The procedure for filling out a tax return (hereinafter referred to as the Procedure for filling out) is also approved by Order of the Ministry of Finance of Russia dated November 7, 2006 N 136n.

Section 2 of the declaration must be completed separately for each foreign person and each lessor. This means that if the obligation of a tax agent arises as a result of relationships with several persons, this section of the declaration is filled out on several pages (clause 23 of the Procedure for filling out a tax return, approved by Order of the Ministry of Finance of Russia dated November 7, 2006 N 136n).

It is not always possible for a tax agent to fill out all the lines in Section 2 of the Declaration. So, in the cases established by paragraphs 1 (purchase of goods from a foreign person), 4 (sale of confiscated property), 5 (sale of goods of a foreign person on behalf of a foreign person), 6 (sale of a vessel) of Article 161 of the Tax Code of the Russian Federation, it is not possible to indicate the taxpayer’s INN and KPP, then in lines 040, 050 of section 2, dashes are placed.

Line 100 is intended to indicate the transaction code, which characterizes the situation where the obligation of a tax agent arises, which, in turn, indicates the procedure for calculating the amount of tax payable. After all, Section 2 of the Declaration does not contain lines to reflect the tax base or tax rate. Tax agent Codes of taxable transactions are listed in the Appendix to the Procedure for filling out the VAT return. To fill out the Declaration, the tax agent will need the information reflected in Section IV “Operations carried out by tax agents.” So, in the case of purchasing goods (work, services) from a foreign person who is not registered for tax purposes in Russia, you must indicate code 1011701.

Organizations (individual entrepreneurs) purchasing goods (work, services) from a foreign person who is not registered for tax purposes in Russia, or leasing property from government agencies, are required to indicate information about the amount of tax in rubles only in line 090. But in the cases provided for paragraphs 4 (sale of confiscated property) and 5 (sale of goods of a foreign person on behalf), the tax agent also fills out lines 110, 120, 130 of section 2 of the Declaration. In this case, the amount of value added tax payable to the budget (line 090) is determined as the sum of the values of lines 110 and 120 minus the indicator of line 130 (clause 24 of the Filling Out Procedure).

The procedure for reflection in accounting tax agent, the amount of tax withheld from the taxpayer's income (subject to withholding) is controversial among specialists, since regulatory documents do not contain detailed rules for this situation. It seems that when resolving this issue, one should take into account the difference between the category of tax agent and the category of taxpayer.

In accordance with subparagraph 1 of paragraph 3 of Article 24 of the Tax Code of the Russian Federation, tax agents are required to correctly and timely calculate, withhold from funds paid to taxpayers, and transfer taxes to the budget system of the Russian Federation to the appropriate accounts of the Federal Treasury. The list of duties of tax agents assumes the sequential performance of each of them:

1. Calculate the amount of tax;

2. Withhold tax from the funds paid;

3. Transfer to the budget.

As you can see, the obligation to pay tax is not assigned to the tax agent, since in accordance with tax legislation, it is the obligation to pay tax that is the main characteristic of the taxpayer (Article 19 of the Tax Code of the Russian Federation).

The taxpayer is obliged to independently fulfill this obligation to pay tax, unless otherwise provided by the legislation on taxes and fees (clause 1 of Article 45 of the Tax Code of the Russian Federation). In particular, in accordance with the Tax Code, the obligation to calculate and withhold tax can be assigned to a tax agent, then the taxpayer’s obligation to pay the tax is considered fulfilled from the moment the tax is withheld by the tax agent (subparagraph 5 of paragraph 3 of Article 45 of the Tax Code of the Russian Federation).

The tax is a mandatory payment levied on organizations and individuals in the form of alienation of funds belonging to them by right of ownership, economic management or operational management (clause 1 of Article 8 of the Tax Code of the Russian Federation). As you can see, tax recognizes the seizure of part of the property that belongs specifically to the taxpayer, and not to third parties. Therefore, the tax agent does not pay the tax instead of the taxpayer, but withholds the amount of tax from funds due to the taxpayer, that is, already owned by the taxpayer.

The objects of accounting are the property of organizations, their obligations and business transactions carried out by organizations in the course of their activities (clause 2 of Article 1 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting”). The debt of an organization is reflected in the accounting accounts only when an obligation arises from this particular organization to other persons.

Please note that the obligation to pay tax does not directly fall on the tax agent. Consequently, obligations to the budget to pay a specific tax are not obligations of an organization recognized as a tax agent. The duty of the tax agent is that he must transfer the withheld amount of tax to the budget within the prescribed period. This means that the obligation to the budget arises at the moment of withholding tax from the taxpayer’s income.

To summarize information on settlements with budgets for taxes and duties paid by an organization, account 68 “Calculations for taxes and duties” is intended (Instructions for the application of the Chart of Accounts for accounting financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n, further Instructions). In this case, account 68 “Calculations for taxes and fees” is credited for the amounts due under tax returns (calculations) for contributions to budgets.

Also, in accordance with paragraph 73 of the Regulations on accounting and financial reporting in the Russian Federation (approved by Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n), any debt other than debt to the budget is reflected on the basis of data from the organization itself, regardless of whether it recognizes the existence debt in the same or different amounts to the other party. But the amounts reflected in the financial statements for settlements with the budget must be agreed upon with the relevant organizations and identical (clause 73 of Order of the Ministry of Finance of Russia N 34n). Identity ensures that the account reflects only those amounts that are declared in the declaration (calculation) for a specific tax.

Taking into account the above, in the accounting of the tax agent, the credit of the account reflects exactly the amount of calculated and withheld value added tax, since on the date of withholding the tax agent’s obligation to the budget arises, which is reported in the corresponding tax return (calculation).

An organization (individual entrepreneur) can deduct the VAT amount, paid to the budget as a tax agent, subject to the fulfillment of the conditions established by Article 171 of the Tax Code of the Russian Federation. Deduction of amounts of VAT paid is provided for not all categories of tax agents. Thus, tax agents who carry out operations specified in paragraphs 4 and 5 of Article 161 of the Tax Code of the Russian Federation do not have the right to deduction, that is, those who sell confiscated property on the territory of Russia and intermediaries involved in settlements in the sale of goods, the transfer of property rights, the performance of work, the provision of services on territory of Russia by foreign persons.

First of all, only the VAT payer can apply the deduction (clause 1 of Article 171 of the Tax Code of the Russian Federation). With regard to the rules for applying a deduction by a tax agent, from January 1, 2009, a new version of paragraph 3 of paragraph 3 of Article 171 of the Tax Code of the Russian Federation is in effect. It is clarified that tax agents have the right to deduct VAT if this tax was paid by them in accordance with Chapter 21 of the Tax Code of the Russian Federation. In this case, as before, goods, works or services purchased by a tax agent must be purchased for use in activities subject to VAT (for the purposes specified in clause 2 of Article 171 of the Tax Code of the Russian Federation).

The conditions for applying the VAT deduction no longer contain a direct indication of the need to withhold tax from the income of the taxpayer (foreign seller, lessor). Such clarification corresponds to the position of the regulatory authorities expressed recently (Letter of the Ministry of Finance of the Russian Federation dated February 28, 2008 N 03-07-08/47, sent for information by Letter of the Federal Tax Service of the Russian Federation dated March 17, 2008 N 03-1-03/908@)). However, the taxation procedure is established by the norms of the legislation on taxes and fees, and the wording of paragraph 3 of Article 171 of the Tax Code of the Russian Federation allowed the courts to come to the conclusion about the legality of refusing to deduct when paying VAT from the tax agent’s own funds (Resolution of the Federal Antimonopoly Service of the Central District of September 19, 2007 N A35-5500 /06-С21).

And the amended paragraph 3 has also been supplemented with an indication of the property rights acquired by the taxpayer from a foreign person who is a tax agent. A number of experts express the opinion that such an addition means an expansion of the use of deductions for VAT paid by tax agents. According to the author, such a statement is premature. Paragraph 3 formulates the conditions for applying the VAT deduction, and the characteristics of the amounts accepted for deduction by taxpayers who are tax agents are contained in paragraph 1 of paragraph 3 of Article 171 of the Tax Code of the Russian Federation. Since paragraph 1 of Article 161 does not require fulfilling the duties of a tax agent in this situation, it cannot be said that the tax was paid by the tax agent “in accordance” with Article 173 and, in general, with Chapter 21 of the Tax Code of the Russian Federation. And this may be grounds for denial of deduction.

In their explanations, tax authorities insist that a tax agent can deduct paid VAT only if he has an invoice, which he himself must issue (Joint Letter of the Ministry of Finance of the Russian Federation and the Federal Tax Service of the Russian Federation dated March 17, 2008 No. 03-1-/908@ ) ,Letter of the Ministry of Taxes of Russia for Moscow dated December 26, 2003 N 24-11/72147 (with reference to the Letter of the Ministry of Taxes of Russia dated April 14, 2003 N 03-1-08/1139/26-N309)). At the same time, in judicial practice there are decisions confirming this position (see Resolution of the Federal Antimonopoly Service of the North Caucasus District dated July 4, 2007 N F08-3941/2007-1558A). In light of this position of the tax authorities, tax agents who are buyers of goods, works, services of a foreign entity or lessees of state property, need to issue an invoice to apply VAT deductions without claims from inspectors. Chapter 21 of the Tax Code of the Russian Federation, as amended before 01/01/2009, did not oblige persons acting as tax agents to issue invoices and register them in the purchase book and sales book. As stated above, the changes made to Article 168 of the Tax Code of the Russian Federation can only strengthen the position of the fiscal authorities.

It seems that the procedure for applying tax deductions is established by Article 172 of the Tax Code of the Russian Federation, and does not depend on the fact that the tax agent has drawn up an invoice. The general conditions for applying the deduction are contained in paragraph 1 of Article 172 of the Tax Code of the Russian Federation. Many experts believe that the provisions of the clause are the same for absolutely all taxpayers regarding the availability of an invoice.

Payment of VAT to the supplier as part of the cost of goods,

Payment of VAT when importing into the customs territory of the Russian Federation,

Payment of VAT to the budget as a tax agent.

Accordingly, in the first case, the tax presented by the supplier is accepted for deduction, in the second case, the tax paid as part of customs duties, in the third case, the tax paid to the budget by the tax agent. An invoice, being a document in which the supplier presents tax to the buyer, can be the basis for applying a deduction only in the first case. In the third case, the basis for applying the deduction is “ document confirming payment of tax amounts withheld by tax agents" The wording of the first paragraph of clause 1 of Art. 172 of the Tax Code of the Russian Federation allows us to conclude that the deduction of VAT amounts withheld by tax agents can be made without invoices on the basis of any other documents confirming the fact of tax withholding and payment. This was confirmed by the Constitutional Court of the Russian Federation in its Determination No. 384-O dated October 2, 2003. The court pointed out that the invoice is not the only document for providing the taxpayer with VAT deductions. A taxpayer who is a tax agent (in particular, a tenant of state property) has the right to receive a deduction on the basis of documents confirming payment of VAT.

Regarding the date of application of the deduction for the amount of VAT paid as a tax agent, there are ambiguous explanations from regulatory authorities.

So in April 2008, specialists from the financial department once again (Letter of the Ministry of Finance of Russia dated September 16, 2005 N 03-04-08/241, Letter of the Ministry of Finance of Russia dated July 15, 2004 N 03-04-08/43) expressed the opinion that the organization that paid to the budget as a VAT tax agent when purchasing services from a foreign entity, has the right to deduct this amount of tax in the tax period in which this amount was actually transferred to the budget (Letter of the Ministry of Finance of the Russian Federation dated 04/07/2008 No. 03-07-08/ 84).

This letter was sent for information to the inspectorate of the Federal Tax Service of the Russian Federation, with the tax service simultaneously communicating its position, which differs from the opinion of the Ministry of Finance of the Russian Federation. Taxpayers insist, as before, that the right to deduction arises for the taxpayer in the next tax period after paying VAT as a tax agent and reflecting the amount of calculated tax in the declaration.

The arguments of the tax service specialists given in the said letter appear to be unfounded. According to the author, in the issue under consideration, arguments with references to the norms of the first part of the Tax Code of the Russian Federation are completely unacceptable. Articles 52 “Procedure for calculating tax”, 55 “Tax period”, 80 “Tax declaration” of the first part of the Tax Code of the Russian Federation determine the values of the corresponding categories in which they are used for tax purposes, but do not establish rules for calculating a specific tax. The procedure for using the right to deduction and the conditions for its provision to the taxpayer are regulated by Chapter 21 of the Tax Code of the Russian Federation. At the same time, the norms of Chapter 21 of the Tax Code of the Russian Federation allow that the right to reimbursement of value added tax from the budget arises in the tax period when the amount of value added tax withheld by the tax agent is actually transferred to the budget. This approach is confirmed in arbitration practice, which is positive for taxpayers.

Thus, in the Resolution of the FAS ZSO dated April 3, 2007 in case No. F04-1851/2007 (32928-A70-31), the court indicated that the procedure for presenting VAT amounts for deduction does not provide for the conditions under which the amount of tax paid in the corresponding tax period can be presented by the payer for deduction only in the next tax period. In this regard, the company, which paid VAT amounts to the budget as a tax agent when purchasing works (services) from foreign persons, legally claimed the right to deduct these tax amounts in the tax period in which it actually paid the tax to the budget. Similar conclusions are contained in the Resolution of the Federal Antimonopoly Service of the North Caucasus District dated May 28, 2008 N F08-2863/2008 in case N A32-24289/2007-59/501 (Determination of the Supreme Arbitration Court of the Russian Federation dated July 25, 2008 N 9235/08 refused to transfer this case to Presidium of the Supreme Arbitration Court of the Russian Federation), Resolution of the FAS Volga-Vyatka District dated 05/02/2007 in case N A43-16382/2006-34-691, Resolution of the FAS North Caucasus District dated 08/21/2008 N F08-4930/2008 in case N A32-3620 /2008-58/49. The tax authority's arguments that the tax agent can deduct VAT only in the period following the time when the tax was paid and reflected in the declaration do not find support among judges (Resolution of the Federal Antimonopoly Service of the West Siberian District dated May 24, 2006 N F04- 3085/2006(22778-A27-26) in case No. A27-34349/05-6, Resolution of the Federal Antimonopoly Service of the Volga-Vyatka District dated July 25, 2005 No. A29-286/2005a, Resolution of the Federal Antimonopoly Service of the West Siberian District dated March 6, 2006 N F04 -2469/2006(20423-A02-40) in case No. A02-3564/2005, Resolution of the Federal Antimonopoly Service of the West Siberian District dated 03/09/2005 N F04-845/2005(9008-A70-14), Resolution of the Federal Antimonopoly Service of the North-Western District dated April 24, 2006 in case No. A13-9766/2005-23).

Thus, a taxpayer who is a tax agent has the right to claim a deduction in the tax period in which settlements with the budget were made, that is, when the agent transferred the tax to the budget.

For failure to fulfill the duties of a tax agent, Article 123 of the Tax Code of the Russian Federation provides for liability in the form of a fine in the amount of 20% of the amount of tax subject to withholding and transfer by the tax agent. Therefore, it is important for an organization (individual entrepreneur) to be able to identify signs of a situation in which, in the absence of a taxable object, there is an opportunity to harm the budget, thereby committing a tax offense and being held accountable.

Literature:

- Tax Code of the Russian Federation (parts I and II).

- Civil Code of the Russian Federation.

- Federal Law of November 26, 2008 N 224-FZ “On Amendments to Part One, Part Two of the Tax Code of the Russian Federation and Certain Legislative Acts of the Russian Federation.”

- Definition of the Constitutional Court of the Russian Federation dated October 2, 2003 N 384-O

- Resolution of the Federal Antimonopoly Service of the North Caucasus District dated July 4, 2007 N F08-3941/2007-1558A

- Resolution of the Federal Antimonopoly Service of the Central District dated September 19, 2007 N A35-5500/06-C21

- Resolution of the FAS ZSO dated April 3, 2007 in case No. F04-1851/2007 (32928-A70-31)

- Resolution of the Federal Antimonopoly Service of the North Caucasus District dated May 28, 2008 N F08-2863/2008 in case N A32-24289/2007-59/501

- Resolution of the Federal Antimonopoly Service of the Volga-Vyatka District dated May 2, 2007 in case No. A43-16382/2006-34-691

- Resolution of the Federal Antimonopoly Service of the North Caucasus District dated August 21, 2008 N F08-4930/2008 in case N A32-3620/2008-58/49

- Resolution of the Federal Antimonopoly Service of the West Siberian District dated May 24, 2006 N F04-3085/2006(22778-A27-26) in case N A27-34349/05-6

- Resolution of the Federal Antimonopoly Service of the Volga-Vyatka District dated July 25, 2005 N A29-286/2005a

- Resolution of the Federal Antimonopoly Service of the West Siberian District dated March 6, 2006 N F04-2469/2006(20423-A02-40) in case N A02-3564/2005

- Resolution of the Federal Antimonopoly Service of the West Siberian District dated 03/09/2005 N F04-845/2005(9008-A70-14)

- Resolution of the Federal Antimonopoly Service of the North-Western District dated April 24, 2006 in case No. A13-9766/2005-23)

- Letter of the Ministry of Finance of the Russian Federation dated 04/07/2008 No. 03-07-08/84

- Letter of the Ministry of Finance of the Russian Federation dated February 28, 2008 N 03-07-08/47

- Letter of the Ministry of Finance of the Russian Federation dated July 3, 2007 N 03-07-08/170

- Letter of the Ministry of Finance of the Russian Federation dated September 16, 2005 N 03-04-08/241

- Letter of the Ministry of Finance of the Russian Federation dated July 15, 2004 N 03-04-08/43

- Letter of the Ministry of Finance of the Russian Federation and the Federal Tax Service of the Russian Federation dated March 17, 2008 No. 03-1-/908@

- Letter from the Ministry of Taxes and Taxes of Russia dated September 24, 2003 N OS-6-03/995@

- Letter of the Department of Tax Administration of Russia for Moscow dated December 26, 2003 N 24-11/72147

In some cases, the taxpayer is not the taxpayer himself, but the company to which he belongs. Often it is this company that pays the taxpayer's wages. The main company, at the same time, pays the tax not from its own pocket, but from funds that rightfully belong to the taxpayer. Therefore, accountants withhold tax from the profit that is due for payment and pay the amount with the VAT amount already calculated.

Who is a VAT tax agent?

At the same time, the company that actually pays the money is called the tax agent. To put it another way, it is she who acts as an intermediary between the company that received the actual profit and the tax service itself, which collects funds and transfers them to the budget. This way of handling money arose due to the fact that some organizations, for legal reasons, are not able to pay taxes on their own.

There are a number of situations in which the state imposes agent duties on a company. They are listed in Article 161 of the RF NU.

In simple terms, an insurance agent is considered to be:

- If you buy foreign-made goods, services or work that are registered in the Russian Federation. Moreover, the place of sale is located in Russia.

- If you rent premises from government agencies, or purchased it.

- If you are selling property that is tied to treasure hunting: coins or other treasure contents, or other wealth.

- If you acquire the property of an organization that has been declared bankrupt.

- If you are an intermediary who sells services or goods whose owners are not located in the Russian Federation.

- If, after the transfer of ownership rights to you, you managed to build a vessel, but did not have time to register it in the International Register of Ships.

What VAT entries are reflected in the tax agent’s accounting?

As for VAT, the accountant uses only two entries:

- Debit 90, Credit equal to 68 - indicates that VAT is charged on the sale of goods and services provided in the main activity of the enterprise.

- Debit 91, Credit equal to 68 - if tax was calculated on the sale of a certain product or service, for additional activities. For example, if a company produces dairy products and simultaneously rents out refrigeration equipment to stores.

Postings for processing input VAT:

- Debit 19, Credit equal to 60 is used to take into account taxes on purchased goods and services.

- Debit 68, Credit 19 is used if VAT on purchased goods and services is accepted for deduction.

To account for input VAT and write it off as expenses, the following entries are used:

- Debit 19, Credit equal to 60 - this scheme is used if VAT on purchased goods is taken into account.

- Debit 19, Credit equal to 60 - an entry that is used if the tax on goods is included in their cost.

In some cases, it is impossible to calculate VAT on a certain group of goods or services. For example, you purchase slot machines that will be used in the gambling business. It is not subject to taxes, so there is nothing to charge VAT on. In such cases, the tax can be calculated into the cost of the machine by hiding it there.

For transactions that are used to recover VAT:

- Debit 60, Credit 68 This entry is used to recover the tax from the advance payment transferred to it. In this case, the reason why VAT is restored does not matter.

- Debit 91, Credit 68 - used to restore VAT on the balance of goods when switching to a special regime, or if a company or enterprise has received tax exemption.

If a tax that was previously accepted for deduction needs to be returned, then a lot depends on the reason for this action

In order for VAT to be transferred to the country’s budget, there is only one entry: Debit 68, Credit 51.

When is VAT paid by the tax agent?

It is necessary to transfer tax to the budget if:

- If the transactions relate to property that belongs to the state.

- If the services are provided by an organization that is registered abroad.

The amount that must be transferred can be calculated in several ways. To calculate the amount of tax on foreign currency payments, it is necessary to correctly determine the transaction rate. Tax agents, who determine the tax base of an enterprise taking into account VAT, assess the tax for payment to the state treasury on the same day when the purchase of goods or receipt of services is made.

How to reflect VAT withholding?

Tax payment is required to be reflected in the financial statements. In order to fill out a VAT declaration to an agent, the issue must be approached with the utmost care and responsibility.

The declaration is submitted in electronic form. This must happen no later than the 25th day of the billing month, or at the end of the quarter.

Attention! Since January 2017, the declaration has been submitted on an updated form, which has been approved by the Federal Tax Service. Be sure to fill out the title page, where you carefully enter all the basic data. Before submitting the form, double-check the cover page.

Next, the agent must fill out paragraphs 1 and 2. If you are not a tax payer, then paragraph 12 will be added to the previous paragraphs. As for paragraph 2, dedicated to agent taxes, they must be filled out separately for each company in relation to which the tax payer considered an agent. This means that if you pay tax not for one organization, but for several, then you will need to fill out all the fields about each of them on a separate sheet.

In paragraph 3, line 180, the tax agent can indicate tax deductions after paying VAT to the country's budget. You can immediately fill out sections 2 and 3 if the purchase of goods or services and the payment of tax on this transaction occurred in the same billing period.

When drawing up a document, the tax agent must rely on the norms for calculating the tax base. The declaration is filled out on the basis of information from the book of sales and purchases, and information obtained from accounting registers.

When does the duty of a tax agent not arise?

But there are a number of situations in which a tax agent ceases to be considered as such. These include:

- If the purchase of property objects and persons who have been declared bankrupt is carried out. For example, if an organization purchases office furniture from a company declared bankrupt.

- In some cases, when concluding a lease agreement.

In such situations, all obligations to pay tax to the treasury are removed from the tax agent, and obligations to pay VAT do not affect his work.

Conditions for tax agent VAT deduction in 2016-2017

VAT paid by the agent can be credited to him. But in order to carry out this procedure, you need to decide on some questions that arise from the situation:

- Is the fact that the agent paid the tax even important?

- Is it necessary to capitalize the object, or is this procedure not necessary?

- Is it worth considering the place where the service was provided?

So, when filing a return as a tax agent, he should be extremely careful. You need to remember that the document must be submitted, like other taxpayers, before the 25th of the current month, or before the end of the billing period.

The declaration is submitted electronically and filled out in any place convenient for you where there is a computer and access to the Internet. Thanks to this service, you no longer need to stand in endless queues wasting time.

The tax agent fills out only the title page and paragraph 2.3 in the declaration. Most often, a tax agent acts as such not for one company, but for several. In this case, when filling out paragraph 2, you will need to work on several sheets, separate for each individual organization.

If the tax agent, for some reason, does not pay tax, or is exempt from it due to the nature of his activity, but at the same time regularly issues invoices to taxpayers, allocating a certain amount of tax, then he will need to fill out additional paragraph 12, in addition to the mandatory first section and title page.

In contact with

For an organization not registered in the Russian Federation, the company acts as a VAT agent (clauses 1 and 2 of Article 161 of the Tax Code of the Russian Federation). Buyers and tenants of the state and (Clause 3 of Article 161 of the Tax Code of the Russian Federation) also act.

At the same time, the departments note that the tax agent receives the right to deduct VAT only after paying the tax to the budget and accepting the purchased goods, works or services for registration (letters of the Ministry of Finance of Russia dated 06.21.13 No. 03-07-08/23545 and dated 11.29.10 No. 03-07-08/334, Federal Tax Service of Russia dated August 12, 2009 No. ShS-22-3/634@).

Also, a mandatory condition for deducting “agency” VAT is an invoice, which the agent issues independently within five calendar days (clause 3 of Article 168 of the Tax Code of the Russian Federation and letter of the Federal Tax Service of Russia dated August 12, 2009 No. ШС-22-3/634@).

How to reflect tax agent VAT in accounting

As a rule, in practice there are no difficulties when recording the tax agent’s VAT in the accounting records. Let's look at the situation using an example.

The company purchased a batch of construction materials from a foreign contractor not registered in the Russian Federation. She will make the following entries in her accounting:

DEBIT 41 CREDIT 60

— goods purchased from the counterparty are accepted for accounting;

DEBIT 19 CREDIT 60

— the amount of VAT under the contract is reflected;

DEBIT 60 CREDIT 68

— VAT is withheld from the amount of payment due to the supplier of goods, works, services;

DEBIT 60 CREDIT 51 (52)

— payment is transferred to the supplier of goods, works, services;

DEBIT 68 CREDIT 51

— “agency” VAT is transferred to the budget;

DEBIT 68 CREDIT 19

— “agency” VAT is accepted for deduction on the tax agent’s invoice.

If the subject of the contract is the performance of work or the provision of services (for example, rental of property), the first accounting entry will have the following form:

DEBIT 20 (26, 44, 91) CREDIT 76

— reflects the accounting expense as of the date of signing the acceptance certificate for work or services, including lease.

Let us note that if a company has entered into an agreement with a foreign counterparty, then the amounts of assets and liabilities must be recalculated for accounting purposes into rubles at the rate valid on the date of the transaction in foreign currency (clauses 4 and 6 of PBU 3/2006 “Accounting for assets and liabilities, the value of which is expressed in foreign currency,” approved by order of the Ministry of Finance of Russia dated November 27, 2006 No. 154n).

What are the consequences of failure to withhold VAT by a tax agent?

Now, if a tax agent does not withhold and transfer the “agency” VAT to the budget, he faces liability under Article 123 of the Tax Code of the Russian Federation - a fine of 20% of the tax amount. Previously, this norm was formulated somewhat differently: from a literal reading of Article 123 of the Tax Code of the Russian Federation, it followed that liability arises if the tax agent did not transfer the tax to the budget.

It is important to remember that before the new edition of the Tax Code of the Russian Federation came into force, some courts declared it unlawful to hold liable a tax agent who failed to withhold tax from a counterparty. Thus, the Federal Antimonopoly Service of the North-Western District, in resolution dated November 17, 2005 No. A26-770/2005-28, recognized the sanctions of tax authorities as unlawful. The fact is that the foreign counterparty received income in kind. And the tax agent was not able to withhold the VAT due for payment to the budget. A similar decision was made by the Ninth Arbitration Court of Appeal in resolution dated September 14, 2012 No. 09AP-25217/2012-AK (upheld by resolution of the Federal Antimonopoly Service of the Moscow District dated December 18, 2012 No. A40-16152/12-90-73).

However, the majority of courts were of the opinion that inspectors have the right to hold a tax agent accountable regardless of whether he withheld the amount of VAT not paid to the budget (decision of the Constitutional Court of the Russian Federation dated 02.10.03 No. 384-O, resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated 28.02.01 No. 5, FAS Volga-Vyatsky dated 02.17.12 No. A43-7281/2011, Uralsky dated 05.11.10 No. Ф09-3355/10-С2 (left in force by the determination of the Supreme Arbitration Court of the Russian Federation dated 09.23.10 No. VAS-10832/10) and North -Kavkazsky dated September 25, 2008 No. F08-5634/2008 (left in force by the determination of the Supreme Arbitration Court of the Russian Federation dated September 23, 2010 No. VAS-10832/10) districts). Now this position is enshrined at the legislative level.

R. Yuropov,

Advisor to the State Civil Service of the Russian Federation, 3rd class

Accountants often ask about tax agent VAT accounting, especially now that books of purchases and sales are submitted along with the declaration. Recently we came across a request from the Federal Tax Service - the VAT return for the 1st quarter of 2015 did not pass logical control, line 180 of section 3 of the VAT return and section 8 “Purchase Book” do not match. I will give an algorithm for the correct accounting of VAT by a tax agent with filling out the necessary sections of the purchase and sales books, as well as the declaration itself. If there are differences in accounting for SCP and BP, I will focus attention.

As an example, let’s take renting premises from a municipal enterprise (MUP). According to the terms of the agreement, we pay the rent. We create the document Write-off from the current account. The counterparty must have the mark “The organization acts as a tax agent for the payment of VAT.

The payment document creates the following transactions:

Based on the document Write-off from the current account, we enter the document invoice issued with the invoice type Tax Agent and Transaction Type Code 06

As you can see, all details and amounts are filled in automatically, provided that the counterparty’s card and payment document are entered correctly. Let's look at the wiring

And SALT according to the score 68.32

Our next operation will be the payment of VAT to the budget. The amount was calculated for us by the invoice issued, and we pay it to the budget. We select Debit Account 68.32, our counterparty, its agreement and the Document for calculating payment for the rental of premises to this counterparty.

Let's look at the wiring

and SALT according to the account 68.32

At the end of the month we carry out the document Receipt of goods and services for rent of premises.

Our document generates the following postings.

Now we move on to filling out the sales book. In BP 2.0 there is no need to create it; when transactions are generated, everything already goes into the sales book and is reflected in the declaration in section 2.

In UPP, we create a sales book in the usual manner at the end of the period. Please note that many accountants think that VAT should be included on the Recovery tab for other transactions, and some even make a “forced” entry in the sales book. In fact, this VAT accrual record appears on the Accrual Payable tab.

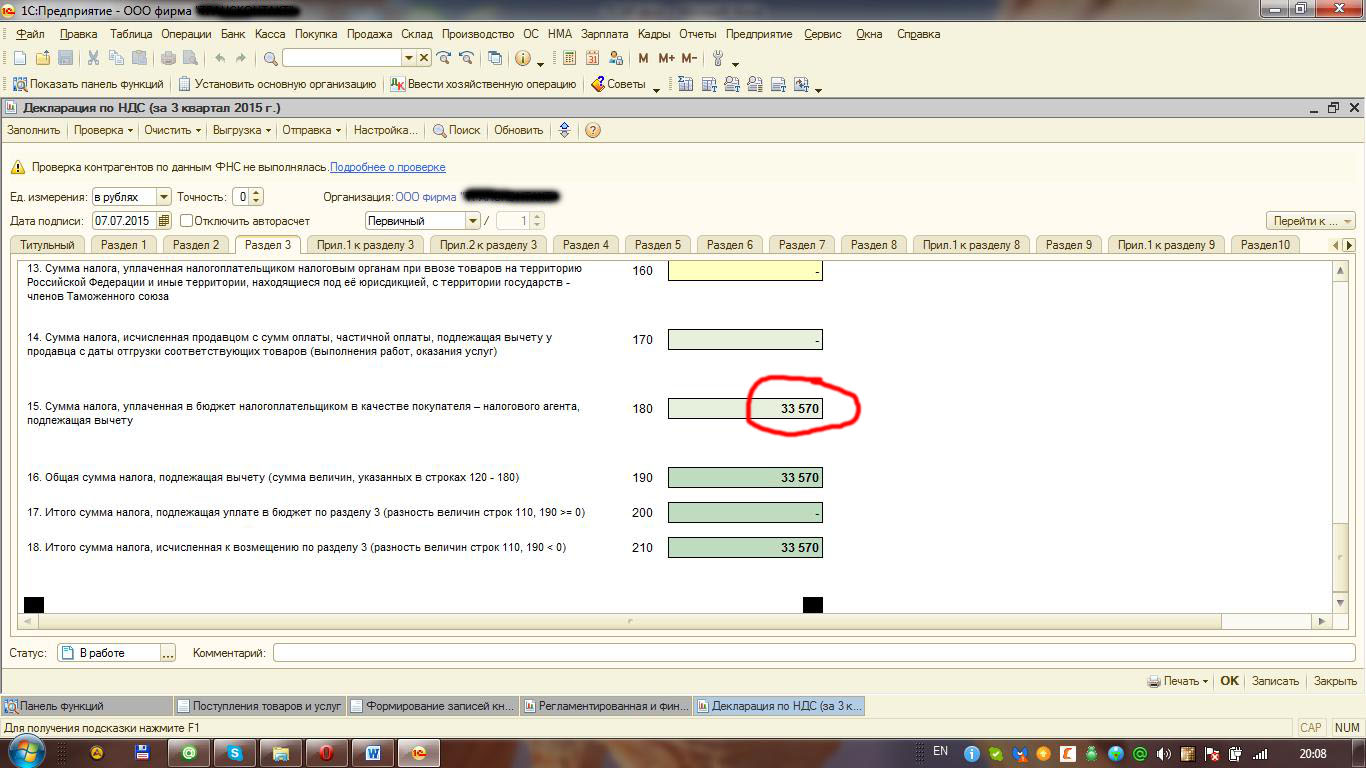

In the declaration, this entry is also displayed in section 2. For each counterparty in a new sheet.Then we move on to creating a purchase book. VAT to be deducted is displayed on the VAT deduction tab by tax agent.

Let's move on to section 9 of the declaration. The deduction for this operation is filled out with the transaction type code 06.

If the sequence of operations is correct, you will not have any problems with tax agent VAT accounting.

About the book “Manuscript found in Zaragoza” Jan Potocki")

- Olesya Novikova: Asian attraction

- What is the difference between fruit drink and compote and juice?

- Broccoli puree soup is both healthy and tasty!

- Yogurt, benefits and harm to the human body. Is yogurt from a yogurt maker healthy?

- Pumpkin jam with orange and lemon: the best recipes

- Reading Psalms in various life situations About help in various everyday needs

- How to make sugar lollipops at home?

- Pumpkin jam: quick and tasty recipes

- Social studies Olympiads for schoolchildren

- “I loved you silently, hopelessly...

- Current problems of the country's economic security

- Who should formulate accounting policies

- Storage Contract for responsible storage accounting and tax accounting

- Insurance premium reporting form

- Who is recognized as a tax agent for VAT (responsibilities, nuances) Postings for VAT tax agent in foreign currency

- Payroll taxes: what the employee pays and what the employer pays, payment terms

- Andrey Kruz, Pavel Kornev About the book “Short Summer” Pavel Kornev, Andrey Kruz

- Robert Kaplan: Your Purpose

- Flowers are always silent read online - Yasya Belaya

- Manuscript found in Zaragoza (Jan Potocki) About the book “Manuscript found in Zaragoza” Jan Potocki