Long-term financial policy(1). Long-term financial policy of the enterprise

Financial strategy involves the formation and use of financial resources to implement the basic strategy of the enterprise and the corresponding courses of action. It allows the economic services of the enterprise to create and change financial resources and determine their optimal use to achieve the goals of the operation and development of the enterprise (Fig.

The importance of this functional strategy lies in the fact that it is in finance that all types of activities are reflected through a system of economic indicators, the balancing of functional tasks occurs and their subordination to the achievement of the main goals of the enterprise. On the other hand, finance is the source, the starting point for developing other functional strategies, since financial resources are often one of the most important limitations on the volume and directions of an enterprise’s activities.

The process of financial management at an enterprise, as a fairly dynamic process, is very sensitive to changes in the external economic and sociopolitical environment (business cycles of the economy, inflation rates, state economic policy, political situation, etc.). The process of justifying and making decisions in the field of finance, including structure and directions entrepreneurial activity, managing debt, dividends and assets is a process strategic management, since it concerns primarily the long-term prospects for the development of the enterprise, and not operational actions. It is in this regard that the heads of economic services of enterprises must be in alliance with the top management of enterprises and participate directly in the development of the general (basic) strategy of the enterprise.

The main tasks of forming the financial strategy of an enterprise are presented in Fig. 6.15.

In a market economy, the development of a financial strategy is preceded by a detailed economic analysis of the functioning of the enterprise, including:

Analysis of the economic activity of the enterprise;

Determination of the financial capabilities of the enterprise.

Analysis of the economic activity of an enterprise makes it possible to assess the efficiency of its activities, reveal bottlenecks and production reserves, determine factors for reducing production costs, increasing profitability, ways to increase labor productivity, the nature of the load and the efficiency of using fixed production assets.

Rice. 6.14. The role of financial strategy in the process strategic planning enterprise development

Rice. 6.15. The main tasks of forming the financial strategy of an enterprise

From the point of view of justification and development of the financial strategy of the enterprise, it is advisable to analyze economic activities in the following main areas:

Assessing the company’s ability to pay short-term obligations;

Assessment of the level (limit) to which the enterprise can be financed with borrowed funds;

Measuring the efficiency of the enterprise's use of the entire complex of its own resources;

Assessing the effectiveness of enterprise management, including the profitability of its activities.

Determining the financial capabilities of an enterprise is determined by assessing its present and future potential in fund formation, the size and sources of implementation of the basic development strategy of the enterprise. Therefore, financial capabilities not only determine the enterprise’s readiness for strategic actions, but also largely determine the nature of these actions. So, for example, with a growth strategy, such financial opportunities as the volume of financial resources in rubles and convertible currency, wear and tear of equipment and a number of others determine the choice of an alternative to the growth strategy: the development of new production, diversification, inter-company cooperation or foreign economic activity.

The main components of the enterprise's financial strategy are presented in Fig. 6.16.

1. Business structure. In accordance with the strategic goals, which are expressed in specific numerical indicators, and the developed basic strategy for the development of the enterprise, its eco-

Rice. 6.16. Main components of an enterprise's financial strategy

nomic services develop the basic principles of financial strategy:

Increasing the assets of the enterprise, including financial resources and rationalizing their structure;

Main directions of profit distribution;

Ensuring enterprise liquidity.

Particular attention is paid to identifying sources of financing, including borrowing opportunities (for example, a special policy for obtaining loans may be justified).

2. Structure of accumulation and consumption. This component of the financial strategy is to optimize the ratio between consumption and accumulation funds, ensuring the implementation of the basic strategy.

3. Debt strategy. It determines the main elements of the credit plan: the source of the loan, the amount of the loan and the schedule for its repayment.

The importance of this component of the financial strategy of an enterprise is determined by the fact that the creditworthiness of an enterprise is one of the main properties of a stable existence in the market. It is for this reason that methods and methods of obtaining loans and repaying them are highlighted in a special debt strategy.

4. Strategy for financing functional strategies and major programs. This component of the financial strategy involves managing the financing of functional strategies and major programs, which does not fit into the annual period. Most often, this strategy includes decisions on capital investments:

For social programs;

To improve and restore existing assets (fixed production assets);

For new construction, acquisitions and acquisitions, R&D, etc.

As a result of the implementation of all components of the enterprise’s financial strategy, a long-term financial plan is developed, which is considered as a synthesizing document that balances all functional strategies, major programs and ensures the achievement of previously developed strategic development goals of the enterprise.

In the process of developing a financial strategy for an enterprise, it is necessary to be guided by three basic principles:

Simplicity;

Consistency;

Security.

The simplicity of the financial strategy of an enterprise suggests that it should be elementary in its construction for perception by all employees of the enterprise, regardless of which department they work in. This allows us to hope that the actions of all employees of the enterprise will be aimed at achieving common goals of its development.

The constancy of the enterprise's financial strategy is due to the fact that in the event of fundamental changes in the implementation process, other functional divisions of the enterprise will not be able to immediately restructure, which will lead to an “imbalance” in the functioning of the enterprise.

The security of an enterprise's financial strategy presupposes that it is designed with a certain “margin of safety”, taking into account possible disturbances in the external environment. The presence of financial reserves and clear coordination of functional strategies means the security of the financial strategy from the point of view of achieving strategic development goals.

The successful implementation of a financial strategy is largely determined by the establishment and development of a financial planning system, including short-, medium- and long-term planning.

Long-term financial planning should include planning for the capital structure and its relatedness. It is closely related to investment planning. The main task of long-term financial planning is to ensure long-term structural balance for the enterprise. This makes it possible to take timely measures if a certain imbalance occurs.

The purpose of structural maintenance of liquidity is to ensure that the enterprise is able to finance its activities by attracting its own and borrowed capital. Potential creditors of an enterprise evaluate it based on the use of special financial indicators, such as, for example, liquidity ratio.

As part of long-term financial planning, a certain balance of plans should be laid down. The financial system of balance sheets for the future is based on investment business projects, calculated taking into account discounted cash flows funds advanced from own and borrowed capitalized resources. Planning the balance sheet structure allows you to assess the financial capabilities of the enterprise and predict at the early stages the potential willingness of creditors to provide borrowed capital.

At the same time, planning the balance sheet structure cannot reflect whether long-term receipts and payments in the field of investment turnover and long-term financing are in equilibrium for the same planning period. For these purposes, long-term balance sheet financing must be supplemented with generalized (integrated) financial planning focused on payment flows.

Long-term financial planning should be supplemented by medium-term planning, which provides for clarification of planned payments and receipts, their volumes and timing.

The approximate structure of the medium-term financial plan is given in table. 6.1.

The medium-term financial plan should have a rolling nature, which focuses on the main flows of payments in the enterprise. This plan should serve as a basis for ensuring current liquidity and complement the long-term financial plan.

Table 6.1

Structure of the medium-term financial plan

| № | Section name | Content |

| 1 | Turnover | This section reflects the main financial flow of the enterprise, which provides current turnover revenues corresponding to its current activities |

| 2 | Current external payments for the enterprise | This section reflects payments of the enterprise that are not directly related to its main activities |

| 3 | Investment activity | This section of the plan reflects receipts and payments from the enterprise’s long-term investment activities |

| 4 | Payments associated with debt financing | This section plans all receipts and payments - paying off debts and obtaining new loans that should occur during the planned period |

| 5 | Payments from non-core activities | In this section, receipts and payments from non-core activities for the enterprise are planned, which affect the results of its functioning |

| 6 | Tax payments | This section reflects planned tax payments |

| 7 | Other payments | This section primarily plans dividend payments for joint-stock companies, as well as possible income from increasing equity capital |

In addition, the medium-term financial plan should provide the opportunity for timely recognition of either a shortage or excess of financial resources in the enterprise.

Many financiers are afraid to talk about financial strategy because this term seems incomprehensible and mysterious to them. The purpose of this article is to destroy the image of mystery and inapplicability in practice and make financial strategy a common tool of financial management.

If you use the concept of “range of proximal development”, then you need to move from the levels “everything is unclear” and “inaccessible to understanding” to the level “understandable with help”, then you will try to draw up a financial strategy for your enterprise and - everything will fall into place!

In polite society one is supposed to start a conversation with a definition. And that's why it's in front of you!

Financial strategy is a model of an organization’s actions to provide financial resources to the organization’s basic strategy. In a simple version, this is a plan for financing the organization’s activities for 3-5 years.

A more complex definition looks like this:

Financial strategy is the implementation of the commercial and operational activities of an organization by financing its current and investment expenses in such a way that a list of key restrictions on the most important parameters of its financial condition is always met. I will describe these most important parameters in detail a little later.

The process of justifying and making financial decisions, namely: determining the structure and directions of business activity, managing liabilities (financing the organization), assets (all property of the organization), dividends - this is a process of strategic management. Why? It determines the long-term prospects for the development of the enterprise.

As a result of the implementation of all components of the organization's financial strategy, a long-term financial plan is developed. It should address all functional strategies and a development plan that ensures the achievement of previously developed strategic goals within the framework of the overall strategy of the organization.

The main task of long-term financial planning is to ensure structural balance. In case of violation, stabilization measures are provided.

Main components of financial strategy:

- Structure of business activity.

- Reserve fund management.

- Asset structure (ratio of non-current and current assets).

- Liability strategy (capital raising).

- Strategy for financing functional strategies and major programs.

- Financial risk assessment.

As a result of using these components of the financial strategy, it is necessary to develop a long-term financial plan. It must integrate and balance functional strategies, major programs, and ensure the achievement of strategic goals approved in the basic strategy.

Each of the components of the financial strategy has its own internal structure.

- 1. Structure of business activity.

- Financing the development plan through the use of equity and borrowed capital. Financing with the help of equity capital occurs either through the distribution of net profit and the allocation of part of it for reinvestment, or through additional contributions from shareholders (owners), or through attracting investors (through the sale of a share in the business with the transfer of funds paid for the share, for development purposes).

- Ensuring liquidity (short-term solvency and managing the dynamics of the residual or market value of assets).

- An increase in assets (property), including an increase in the monetary component of assets, improvement (optimization) of the asset structure.

- Reserve fund management.

Business is supposed to be conducted with a reserve. Lack of financial reserves is one of the most common financial management problems.

A reserve fund is created during a favorable period, and spent during a crisis.

There are three ways to set the amount of the reserve fund in real money.

A) Reserve fund\Assets=10 (20)%.

B) Reserve Fund\Revenue=5%.

C) Reserve fund = amount of payments for 5 (15) days.

- Asset structure.

The profitability of a business depends on the ratio of non-current and working capital. If in production organization non-current assets relate to current assets as 7 to 1, then we can immediately assume that the profitability of the business is low (or zero) and, most likely, the prospects are bleak.

- Capital raising strategy.

- Determination of the structure of liabilities (capital) in the form of the “own/borrowed” ratio.

The point of business is to use equity capital (SC), for which dividends are paid to shareholders (owners). With high business profitability (return on sales on net profit of more than 10%), it becomes possible to attract borrowed bank capital (BC). In this case, by paying the bank 9-15% for loan money, there is an opportunity to earn a little more on this capital, thereby increasing the return on equity capital. That is why the correct SK/ZK ratio should be 3/1.

- Determining the timing of capital raising.

Priority, of course, is given to long-term borrowed capital, while long-term capital is considered to be capital raised for a period of 3 years or more. Lending for short periods is usually a necessary measure due to the phenomenon of high risk of issuing a “long” loan from the bank’s point of view.

- Determination of the cost of capital: (dividends + interest on loans)/liabilities.

- Determination of the structure of liabilities (capital) in the form of the “own/borrowed” ratio.

The organization's ability to attract additional capital is assessed through its financial potential. It lies in the organization’s ability to accumulate the maximum amount of capital (cash), with given parameters of the cost of capital, the optimal timing of its attraction and the level of risk.

Example: to maintain market share and level of competitive advantage, it is necessary to implement a development program, and for this the organization required additionally attract (borrow) 150 financial units, while there is a possibility additionally attract 80 financial units in the form of loans. At the same time, with an increase in debt by 80 units, the capital structure (equity/debt capital ratio) will become 1/5. This ratio of equity/borrowed capital will lead to the fact that most of the net profit will be spent on paying interest on loans. It is not possible to repay so many loans within 3-4 years. The payment of dividends will become impractical, the value of the organization will begin to slowly decrease. The business will become unsuccessful (in terms of the level of return on invested capital). The likelihood of a breakthrough and victory in a competitive competition when investing in the development of 150 units is assessed as low. The recommendation is to give up the fight with the market leader and agree that over the next 3 years the organization’s market share will decrease while maintaining the same revenue volume. Next, focus on improving your financial condition, return most loans, accumulate reserves and wait for a crisis in the economy, in which the market leader goes bankrupt due to a risky financial strategy, and at this moment increase marketing activity using accumulated reserves.

As can be seen from the above example, financial strategy is closely related to competition and is aimed at changing the key financial parameters of the organization over the long term.

Let's move on to the strategy for financing functional strategies and major programs.

It is useful to develop strategies for the main functions: marketing, production, personnel management, logistics. For each function, its own functional strategy is developed, and its financing should be reflected in the financial strategy. Major programs usually affect all major functions of the organization, they are usually the leading core strategy of the organization and therefore their funding is considered in the form of a separate financial plan.

Financial strategy has its own principles:

Simplicity

Still, the financial strategy should be simple and understandable to all employees. For example, “our organization is the best in the country in terms of cost savings, so we have the opportunity to develop using our own accumulated funds”.

Constancy

Constancy is due to the fact that strategic business processes are inertial, and their continuous restructuring and frequent changes in strategic business parameters are associated with a loss of business efficiency.

Of course, a small trading company with 70 employees and revenue of 340 million rubles a year at first glance can often make rapid maneuvers. But the practice of observing even such small companies shows that forced rapid changes most often “turn” the organization towards a worse state, and the organization takes years to achieve some progress. The larger the scale of the business, the more long-term planning is required. A large machine-building enterprise, in order to develop its competitive advantages (or to maintain them), is forced to innovate and develop development programs for 5-10 years in advance. And for such a large organization in size and scale, rapid changes are contraindicated.

Security

The financial strategy must be designed with an established margin of safety, which should allow the key parameters of the strategy to be maintained with minor changes in the parameters of the external environment. The onset of a financial or any other crisis must be foreseen within the framework of the overall strategy; the financial strategy must have in its structure a description of several options for “Plan B” (on average for the scale of the business - this can be done in abstract), which should be switched to when, for example, a decrease in revenue (or a drop in prices) by 10-15%.

Reliability and stability are easiest to maintain with the help of financial reserves and with the help of decisions to reduce (reduce the dynamics) of the development program.

Fragment of the financial strategy of a large metallurgical company:

“The key priorities of our financial strategy

Strong financial position - a significant liquidity reserve, low debt burden and a balanced structure of the debt portfolio.

NLMK has a significant reserve of cash liquidity and undrawn credit lines. The company's liquid funds significantly exceed its short-term debt.

A comfortable level of debt burden during all periods of the cycle has always been one of NLMK’s priorities. Despite capital-intensive growth during recent years, NLMK remained a company with one of the lowest debt loads among metallurgical companies in Russia and the world. NLMK plans to gradually reduce its debt burden in the future and sets a goal to reduce the net debt/EBITDA ratio to 1.0x.

The structure of the debt portfolio and the debt repayment schedule are currently comfortable for us. Over the past two years, we have actively managed our debt portfolio and, thanks to access to the Russian and international capital markets, have restructured it towards financial obligations with longer maturities and lower interest rates.”

Source: http://nlmk.com/ru/investor-relations/financial-strategy

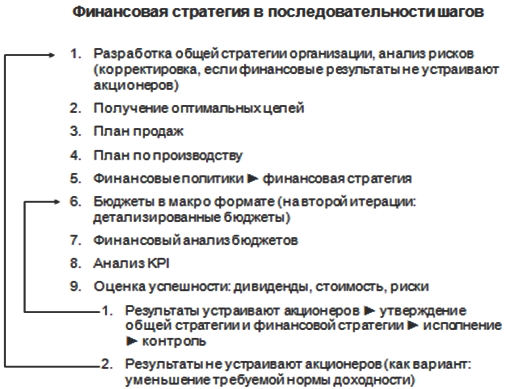

If we talk about a simple sequence of steps aimed at developing a financial strategy, then below is one of possible options such a sequence, optimized for medium-sized businesses.

| Name of the seminar, training, course | Apr | May | Jun | Jul | Aug | Price, rub. |

| - | - | - | - |

05-06 |

28 200 | |

| - | - | - |

15-16 |

- | 29 900 | |

| - | - |

06-07 |

- | - | 28 200 | |

|

24-25 |

- | - | - | - | 29 900 | |

| - |

22-23 |

- | - | - | 29 900 | |

| - | - | - | - |

07-21 |

19 850 | |

| - | - | - | - |

19-21 |

38 100 | |

| - |

29-31 |

- | - | - | 38 100 | |

| - | - |

20-21 |

- | - | 28 200 | |

| - | - | - |

31-01 |

- | 28 200 | |

|

03-04 |

- | - | - | - | 28 200 |

Forecasting the balance sheet using the percentage of sales method

4.1 Essence, goals and objectives of financial planning

Corporate financial planning is the financial planning of the activities of business entities.

Financial planning is the process of developing and adopting quantitative and qualitative targets in the area financial relations and determining the ways to most effectively achieve them.

Requirements for corporate financial planning are reflected in regulations regulating the activities of business companies, the procedure for issuing securities, as well as standards of corporate conduct.

Requirements for the corporate financial planning system

| Directions of Requirements | Contents of requirements |

| requirements for the content of financial policy | financial policy should include dividend policy, accounting policy, investment policy, policy for financing current assets |

| requirements for the composition of financial plans | The financial plan should include: an investment plan; cash flow plan; planned balance sheet of assets and liabilities; income and expense plan; loan repayment plan |

| requirements for financial planning methodology | development of multivariate forecasts, risk analysis of the implementation of developed plans. availability of practice of clarifying forecasts of the internal and external environment at least once a quarter; planning actions in case negative influences environmental factors on the results of the enterprise's activities disclosure of planned information that does not contain trade secrets on a website on the Internet |

| requirements for organizing financial planning | The Board of Directors approves the enterprise development strategy. The Board of Directors annually approves the financial and economic plan and the practice of reporting on the implementation of the financial and economic plan. |

The main goal of financial planning on modern stage consists in justifying the company's strategy in commodity, financial, information and other markets for the upcoming economic period from the standpoint of an economic compromise between profitability, liquidity and risk, as well as in determining the required amount of financial resources within optimal structure capital.

The objectives of financial planning are:

determining the need for financial resources and directions for their effective use;

determination of the rational structure and volume of funding sources;

balancing expected cash receipts and expenditures;

assessment of the effectiveness of the production and economic activities of the enterprise and its divisions in the planning period from the point of view of final financial results;

providing information to evaluate the effectiveness of investment projects.

Financial strategy and financial policy of the enterprise

Financial strategy is a system of long-term financial goals of an enterprise and the most effective ways to achieve them.

Being part of the overall strategy for the economic development of an enterprise, the financial strategy is subordinate to it and must be consistent with its goals and directions. At the same time, the financial strategy itself has a significant impact on the formation of the overall strategy for the economic development of the enterprise.

Financial strategy includes:

Strategy for the formation of financial resources;

Investment strategy;

Strategy for ensuring the financial security of the enterprise;

Strategy for improving the quality of financial management of an enterprise.

In the process of developing a financial strategy, the financial policy of the enterprise is determined.

Financial policy is a document reflecting the principles and approaches to implementation financial activities enterprises.

In contrast to the financial strategy as a whole, financial policy is formed only in the control areas of the enterprise’s financial activities, which require ensuring the most effective management to achieve the main strategic goal of this activity.

There are short-term and long-term financial policies.

Short-term financial policy includes:

Accounting and tax policies;

Working capital management policy;

Depreciation policy;

Credit policy;

Pricing policy.

Long-term financial policy consists of dividend policy and investment policy.

| Policy direction | Content |

| Dividend policy | 1. Principles and rules for paying dividends 2. The rate of distribution of net profit for dividends 3. Methodology of dividend payments 4. Form of payment of dividends |

| Investment policy | 1. Principles and rules of investment activity 2. Priority areas of investment 3. Requirements for the efficiency and risk of investment projects |

| Accounting policy | 1. Principles and rules of conduct accounting 2. The procedure for recording the acquisition of materials in accounting 3. The method for assessing inventories released into production The method for calculating depreciation Types of reserves created The procedure for accounting for production costs and the formation of financial results |

| Depreciation policy | 1. Principles and rules of calculation depreciation charges 2. Method of calculating depreciation for tax and accounting 3. Approach to determining the useful life of used property 4. Determining the feasibility of revaluing depreciable property 5. Determining the possibility of using correction factors to depreciation rates 6. Limit for classifying objects as depreciable property |

| Price policy | 1. Principles and rules for setting prices for products sold, works and services 2. Characteristics of the elasticity of demand prevailing in the product market 3. Approaches to determining the level of profit in the price of products 4. Approaches to providing discounts on prices |

| Policy for managing current assets and liabilities | 1. Principles and rules for managing current assets and liabilities 2. approach to the formation of stocks of raw materials and materials 3. Approach to the formation of inventories finished products in the warehouse 4. Approach to determining the minimum required balance of cash and cash equivalents 5. Preferences in choosing sources of financing 6. Criteria for choosing between receiving a deferred payment and a discount on the price of materials |

The development of a financial strategy is carried out, as a rule, collectively at the highest level of management and approved by the owners of the enterprise.

The formation of financial policy can be multi-level. At a large enterprise, the chief accountant, financial director, CEO and representatives of owners.

Financial plans are quite complex both in structure and content. Therefore, their development requires the efforts of various departments of the enterprise (financial department, economic planning department, marketing department, accounting department, logistics department, sales department, chief mechanic department, chief power engineer department, capital construction department, production divisions, etc. .). Responsibility for the development of financial plans rests with the financial and economic services of the enterprise.

4.3 System of financial plans of the enterprise. Financial section of the enterprise business plan

A financial plan is a document that reflects the desired parameters of income, expenses, financial condition, cash receipts and payments of the planning object and how to achieve them.

| Types of financial plans | Content | |||

| Long-term and medium-term financial plans | ||||

| 1.1 Profit and loss plan | Planned indicators for two, three or more years, income, expenses and financial results of the organization | |||

| 1.2 Investment plan | Plan for two, three or more years of directions and amounts of capital investments and other investments, as well as sources of their financing | |||

| 1.3 Planned balance of assets and liabilities | Plan for two, three or more years of the amount of assets and liabilities of the enterprise according to enlarged items | |||

| 1.4 Plan of cash receipts and payments | Plan for two, three or more years of cash receipts and payments under consolidated items | |||

| 2. Annual financial plans | ||||

| 2.1 Profit and loss plan | Calculation of the financial results of the enterprise for the planned year with a quarterly or monthly breakdown | |||

| 2.2. Planned balance sheet of assets and liabilities | The size of assets and liabilities of the balance sheet at the end of the plan year | |||

| 2.3 Planned balance of cash receipts and payments | Amount, sources of cash receipts, amount and directions of expenditure of funds with a quarterly or monthly breakdown | |||

| 2.4. Investment plan | Annual plan for capital investments and other investments, as well as sources of their financing | |||

| 3. Operational financial plans | ||||

| 3.1 Tax calendar (tax payment plan) | The size and timing of tax payments of the enterprise for the upcoming quarter (month) | |||

| 3.2. Payment calendar (balance of cash receipts and payments) | Monthly cash flow plan in cash and non-cash form broken down by ten days (five days, days) | |||

| 3.3 Credit plan | Plan for the amount and timing of loan interest payments and principal payments | |||

| 3.4. Cash plan | Cash flow plan through the enterprise's cash desk indicating specific timing of cash requirements | |||

The final section of any business plan is the financial section. The content of this section depends on the purpose of developing a business plan and its purpose.

Typical contents of the financial section of a business plan include:

1. Forecast of sales volumes;

2. Plan of income and expenses;

3. Balance of cash receipts and payments;

4. Consolidated balance sheet plan of assets and liabilities of the enterprise;

5. Break-even analysis, sensitivity analysis;

6. Financing strategy.

Forecast of sales volumes is compiled based on the data from the previous sections of the business plan. It reflects the planned sales amounts for each product in monetary terms. The forecast of sales volumes, as a rule, is drawn up for 3 years, for the 1st year broken down by month, for the 2nd year with a quarterly breakdown, for the 3rd year in the total amount for the year.

To calculate the final financial results, a income and expense plan, on the basis of which the profit of the 1st year is forecast monthly, the 2nd year quarterly and the 3rd year as a whole.

Purpose of compilation balances of cash receipts and payments– achieve synchronicity between the receipt of funds and their expenditure. By drawing up this balance sheet, you can assess how much and when money needs to be invested in the business and from what sources the necessary amounts of money will be received.

Balance sheet of assets and liabilities reflects the state of the enterprise’s property and the sources of its formation as of a certain date. The forecast balance is drawn up as usual balance sheet, where the values of assets and liabilities are indicated at the beginning and end of the planning period, but with less detail in the items. When drawing up a balance sheet, a balance of assets and liabilities is achieved, and it may be necessary to make corrections to all other calculations.

To assess the risk of the project, carry out sensitivity analysis. To do this, select indicators for which the risk is high and, by setting a step-by-step change in these indicators at a certain interval, determine the impact of their changes on other financial indicators. Break-even analysis is based on calculating the project's profitability threshold and its margin of financial strength.

The final part of the financial section of the business plan reflects project financing strategy. This part answers the following questions:

1. How much total funds are needed?

2. Where and in what form are these funds expected to be received?

3. When can we expect full repayment of borrowed funds and investors receiving income?

4. What is the amount of income received by investors?

Particular attention is paid to assessing the economic efficiency of project implementation.

4.4 Methods of financial planning and forecasting in an enterprise.

Methods financial planning is a set of techniques and methods by which the development and justification of planned financial documents is ensured.

Methods of financial planning and forecasting can be divided into three groups:

methods based on the use of knowledge, intuition and experience of specialists;

formalized methods;

Combined.

The methods of the first group used in financial planning include

method of expert assessments;

Delphi method

Scripting method.

These methods are used when specialists cannot verbal description transfer the task at hand into a formal one or do not have the appropriate resources for this.

Expert assessment method involves obtaining the required information by interviewing and processing expert opinions in a special way.

The method of expert assessments is quite valuable in financial planning carried out in an unstable environment and is used in determining financial strategy, directions of financial policy, evaluating draft financial plans, forecasting sales volumes, inflation indices, exchange rates, costs for new projects, etc.

The essence of the Delphi method consists in obtaining information through sequential individual questioning of experts and integrating their opinions into a single one. In this case, several rounds of expert interviews are conducted. This method is focused on making various kinds of forecasts and assessing the likelihood of a particular event occurring. Its use is most relevant when developing a financial strategy for an enterprise.

Scripting method based on the development and analysis of documents containing a description of the problem and proposals for its solution. The scenario provides not only meaningful reasoning that helps not to miss details that cannot be taken into account in a formal model, but also, as a rule, contains the results of economic and statistical analysis with preliminary conclusions. This method is used in the formation of long-term and medium-term forecasts of financial indicators, in the formation of the financial strategy and financial policy of the enterprise.

Formalized methods are based on the use of mathematical, economic-mathematical and graphical methods and models.

Toward formalized methods used in financial planning include

direct counting method:

factor method;

method of proportional dependencies;

normative;

balance;

optimization methods;

statistical methods;

graphical methods

Direct counting method involves the use of certain non-random functional relationships between various technical, economic and financial indicators.

To calculate the target indicator, an equation is used that has the following form:

y = f* (X1,X2…Xn); (7.1)

X1,X2…Xn – planned values of indicators that affect the desired one;

f is a strictly determined functional dependence.

For example, to determine revenue (the required indicator), it is necessary to multiply the indicators that affect revenue (sales volume and price)

This method is actively used in annual and operational financial planning and is quite accurate, provided that it is reliable to determine the planned values of indicators that affect the desired one.

Essence factor method is the calculation of financial indicators based on changes in the basic value of the indicator under the influence of a number of factors /32/.

Stages of planning using the factorial method

1. the basic value of the indicator (Vo) is determined;

2. factors are determined that will affect the change in the indicator in the planning period X1,X2...Xn,;

3. the form of dependence of the indicator on the selected factors is determined (f* X1, f* X2… f* Xn);

4. the values of factors in the planning period are predicted

5. The change in indicator U1, U2….Un is assessed

6. The planned value of the indicator is calculated

Up = Uo + U1 + U2 +…. +Уn, (7.2)

The basis of the proportional dependence method constitutes the thesis that it is possible to identify a certain indicator that is the most important from the point of view of the characteristics of the company’s activities, which, thanks to this property, could be used as a base for determining the forecast values of other indicators in the sense that they are “tied to the base indicator using the simplest proportional dependencies" /7/. As a basic indicator, most often, either revenue from product sales or cost is used.

y = A*X, (7.3)

where y is the planned value of the desired indicator;

X – reporting value of this indicator;

A is the growth index of the indicator taken as the base one.

This method has become widespread due to the fact that it allows planning with extremely limited information.

The essence of the normative method is the calculation of financial indicators by multiplying norms by the planned value of the economic indicator in relation to which the norm is established /1/.

The planned indicator is calculated using the formula:

y = H*X; (7.4)

where y is the planned value of the desired indicator;

N – established norm;

X is the planned value of the indicator in relation to which the norm is established.

Balance sheet method involves the calculation of planned indicators based on comparison and mutual coordination of receipts and expenditures of financial resources /32/. Financial planning uses a cost balance, which is developed in monetary terms.

The balance method is used to distribute financial resources according to areas of use and determine the need for external financing.

The balance sheet looks like this:

O N + P = P + O K, (7.5)

Where HE– balance of funds at the beginning of the planning period, rub.;

P– receipt of funds, rub.;

R– expenditure of funds, rub.;

OK- balance of funds at the end of the planning period, rub.

Essence optimization method is that the planned value of the indicator is determined as a result of solving the optimization problem /33/.

The choice of the optimal option is made based on the accepted selection criterion.

Such criteria could be:

1) minimum reduced costs

2) maximum present profit

3) maximum income per ruble of invested capital;

4) minimum duration of one revolution in days, i.e. maximum capital turnover rate;

5) minimum financial risk;

6) other criteria (maximum level of profitability, etc.)

Statistical methods are used if it is not possible to represent the system in the form of deterministic categories, but it is possible to display it using random events that are described by probabilistic characteristics and statistical patterns.

The category of statistical methods used in financial planning includes methods for processing spatial, temporal and spatiotemporal aggregates /7/.

Graphical methods - methods for determining planned indicators as a result of plotting schedules. For example, using a graphical method, you can calculate the volume of production and sales of products at which the enterprise has neither profit nor loss.

Situational modeling refers to combined methods of financial planning, since the intuition and experience of specialists are used to select situational variables and predict their values, and the dependencies between these variables are described, as a rule, in a formalized language.

This method is based on models designed to study the influence of different values of situational variables on the desired financial indicators /32/.

4.5 Budget planning. Types of financial budgets.

Currently, annual and operational financial planning is closely linked to the budgeting process.

Budgeting – is a technology for financial planning, accounting and control of income and expenses received from business at all levels of management, which allows you to analyze predicted and obtained financial indicators /7/.

Budget- this is, as a rule, a short-term financial plan that reflects the income, costs and results of the production and economic activities of the enterprise expressed in monetary terms.

The financial budgets of an enterprise include:

Budget of income and expenses;

Cash flow budget;

Investment budget;

Budget balance.

Budget of income and expenses involves comparing all the income and expenses of the enterprise for the budget period, highlighting the most important (critical) items of expenses and sources of income. The main objective of this budget is to show the company’s management the effectiveness of economic activities for the coming period.

Send your good work in the knowledge base is simple. Use the form below

Students, graduate students, young scientists who use the knowledge base in their studies and work will be very grateful to you.

Posted on http://www.allbest.ru/

INconducting

capital financial planning dividend

Financial policy is a fundamental element in the financial management system at both the macro and microeconomic levels. When organizing financial relations for the distribution, redistribution and use of gross domestic product and national income, the state determines the main goals and objectives facing society and, accordingly, the financial system country, all its spheres and links.

Financial policy is the determination of goals and objectives to achieve which the process of formation, distribution and redistribution of the gross domestic product is directed to provide financial resources for the continuous reproduction process and the solution of individual social, economic and political problems of society.

The main goal of financial policy is to create financial conditions for the socio-economic development of society, improving the level and quality of life of the population. Achieving this goal is possible only with the effectiveness of specific forms of distribution, redistribution and use of the available financial resources of society and the financial potential of the state.

The state, represented by the legislative (representative) and executive power is the main subject of the ongoing financial policy. It develops a strategy for the main directions of financial development for the future, determines action tactics for the coming period, and determines the means and ways to achieve strategic objectives. Subjects of financial policy are also local governments, organizations different forms property.

The objects of financial policy are monetary relations on the formation, distribution and use of funds of funds in all areas and links of the financial system.

Financial strategy is a long-term course of financial policy, designed for the long term and providing for the solution, as a rule, of large-scale problems.

Financial tactics are methods for solving financial problems in the most important areas of financial strategy.

Financial policy strategy and tactics are interconnected.

1. Long-term financial policy of the enterprise

1.1 Concepts and goals of long-term enterprise policy

Financial policy of the enterprise- a set of measures for the purposeful formation, organization and use of finances to achieve the goals of the enterprise.

Financial policy- the most important compound element general enterprise development policy, which also includes investment, innovation, production, personnel, marketing, etc. policies. If we consider the term « policy » more broadly, it is “actions aimed at achieving a goal.”

Thus, the achievement of any task facing an enterprise is, to one degree or another, necessarily connected with finances: costs, income, cash flows, and the implementation of any solution, first of all, requires financial support.

Thus, financial policy is not limited to solving local, isolated issues, such as market analysis, developing procedures for passing and approving contracts, organizing control over production processes, but is comprehensive.

Long-term financial policy framework- a clear definition of a unified concept for the development of the enterprise in the long term, the choice of optimal mechanisms for achieving set goals, as well as the development of effective control mechanisms.

The main purpose of creating an enterprise- ensuring maximization of the welfare of the owners of the enterprise in the current period and in the future. This goal is expressed in ensuring the maximization of the market value of the enterprise, which is impossible without the effective use of financial resources and building optimal financial relations both within the enterprise itself and with counterparties and the state.

To achieve the main goal of financial policy, it is necessary to find the optimal balance between strategic directions:

1. profit maximization;

2. ensuring financial stability.

The development of the first strategic direction allows owners to receive income on invested capital, the second direction provides the enterprise with stability and security and relates to risk control.

Developing a financial strategy involves certain stages:

· critical analysis of previous financial strategy;

· justification (adjustment) of strategic goals;

· determining the timing of the financial strategy;

· specification of strategic goals and periods for their implementation;

· distribution of responsibility for achieving strategic goals.

It is always a search for balance, the currently optimal relationship between several areas of development and the choice of the most effective methods and mechanisms for achieving them.

The financial policy of an enterprise cannot be unshakable, determined once and for all. On the contrary, it must be flexible and adjusted in response to changes in external and internal factors.

One of the basic principles of financial policy is that it should be based not so much on the actual situation as on the forecast of its changes. Only on the basis of foresight does financial policy become sustainable.

Long-term financial policy- the basis of the financial management process of an enterprise. Its main directions are determined by the founders, owners, and shareholders of the enterprise. However, the implementation of long-term financial policy is possible only through the organizational subsystem, which is a set of individuals and services that prepare and directly implement financial decisions.

They implement long-term financial policies at enterprises in different ways. This depends on the organizational and legal form of the business entity, the scope of activity, as well as the scale of the enterprise.

The subjects of management in small enterprises can be the manager and the accountant, since small business does not imply a deep division of management functions. Sometimes external experts and consultants are brought in to adjust development directions.

In medium-sized enterprises, current financial activities can be carried out within other departments (accounting, economic planning department, etc.), while serious financial decisions (investing, financing, long-term and medium-term distribution of profits) are made by the general management of the company.

In large companies it is possible to expand the organizational structure, personnel composition and clearly differentiate powers and responsibilities between:

· information bodies: legal, tax, accounting and other services;

· financial authorities: financial department, treasury department, securities management department, budgeting department, etc.;

· control bodies: internal audit, audit.

As a rule, the financial director is responsible for posing financial problems and analyzing the feasibility of choosing one or another method of solving them. However, if the decision being made is significant for the enterprise, he is only an adviser to senior management personnel.

When developing and implementing long-term financial policy, enterprise management is forced to constantly make management decisions from many alternative directions. Timely and accurate information plays a vital role in choosing the most profitable solution.

Information support for the financial policy of an enterprise can be divided into two large categories: formed from external sources and internal ones.

Fromexternal sources:

1. Indicators characterizing general economic development

countries:

· growth rate of gross domestic product and national income;

· volume of money emission in the period under review;

· cash income of the population;

· household deposits in banks;

· inflation index;

· central bank discount rate.

This type of informative indicators serves as the basis for analyzing and forecasting the conditions of the external environment of the enterprise when making strategic decisions in financial activities. The formation of a system of indicators for this group is based on published state statistics.

2. Indicators characterizing the financial market situation:

· types of main stock instruments (shares, bonds, etc.) traded on the exchange and over-the-counter stock markets;

· quoted supply and demand prices of the main types of stock instruments;

· lending rate of individual commercial banks.

The system of normative indicators of this group serves to make management decisions when forming a portfolio of long-term financial investments, when choosing options for placing free funds, etc. The formation of a system of indicators for this group is based on periodic publications of the Central Bank, commercial publications, as well as official statistical publications.

3. Indicators characterizing the activities of counterparties and competitors.

A system of informative indicators of this group is necessary mainly for making operational management decisions on certain aspects of the formation and use of financial resources.

4. Regulatory indicators.

The system of these indicators is taken into account when preparing financial decisions related to the peculiarities of state regulation of the financial activities of enterprises. The sources for the formation of indicators of this group are regulations adopted by various government bodies.

Frominternal sources, divided into two groups.

1. Primary information:

· accounting reporting forms;

· operational financial and management accounting.

The system of informative indicators of this group is widely used by both external and internal users. It is applicable in financial analysis, planning, development of financial strategy and policy on the main aspects of financial activity, and gives the most aggregated picture of the results of the financial activity of the enterprise.

2. Information obtained from financial analysis:

· horizontal analysis (comparison of financial indicators with the previous period and for several previous periods);

· vertical analysis (structural analysis of assets, liabilities and cash flows);

· comparative analysis(with industry average financial indicators, competitor indicators, reporting and planned indicators);

· analysis of financial ratios (financial stability, solvency, turnover, profitability);

· integral the financial analysis and etc.

Thus, for the successful implementation of the enterprise’s long-term financial policy, management must, firstly, have reliable information about the external environment and predict its possible changes; secondly, have information about the current parameters of the internal financial situation; thirdly, systematically carry out an analysis that makes it possible to obtain an assessment of the results of economic activity of its individual aspects, both statically and dynamically.

1.2 Cost of main sources of capital

Often the term "capital" is used in relation to both sources

funds and assets. With this approach, when characterizing sources, they talk about “passive capital”, and when characterizing assets, they talk about “active capital”, dividing it into fixed capital (long-term assets, including construction in progress) and working capital (this includes all current assets).

Capital- these are the means that a business entity has at its disposal to carry out its activities in order to make a profit.

The enterprise's capital is formed both from its own (internal) and from borrowed (external) sources.

The main source of funding is equity. It consists of authorized capital, accumulated capital (reserve and added capital, accumulation fund, retained earnings) and other income (targeted financing, charitable donations, etc.).

Authorized capital- this is the amount of funds of the founders to ensure statutory activities. At state-owned enterprises, this is the value of property assigned by the state to the enterprise with the rights of full economic management; at joint-stock enterprises - the nominal value of all types of shares; for limited liability companies - the sum of the owners' shares; for a rental enterprise - the amount of contributions of its employees.

The authorized capital is formed in the process of initial investment of funds. Contributions of founders to the authorized capital can be in the form of cash, property and intangible assets. The amount of the authorized capital is announced upon registration of the enterprise and when adjusting its value, re-registration of the constituent documents is required.

Added capital as a source of funds for an enterprise, it is formed as a result of the revaluation of property or the sale of shares above their nominal value. Savings Fund is created from the profit of the enterprise, depreciation charges and the sale of part of the property.

The main source of replenishment of equity capital is the profit of the enterprise, at the expense of which accumulation, consumption and reserve funds are created. There may be a balance of retained earnings, which, before its distribution, is used in the turnover of the enterprise, as well as the issue of additional shares.

Funds for special purposes and targeted financing- these are gratuitously received values, as well as irrevocable and repayable budgetary allocations for the maintenance of social and cultural facilities and for restoring the solvency of enterprises that receive budgetary financing.

Borrowed capital- these are loans from banks and financial companies, loans, accounts payable, leasing, commercial paper, etc. It is divided into long-term (more than a year) and short-term (up to a year).

Any organization finances its activities, including investment, from various sources. As payment for the use of financial resources advanced to the organization’s activities, it pays interest, dividends, remuneration, etc., i.e. bears some reasonable costs to maintain its economic potential. As a result, each source of funds has its own value as the sum of the costs of providing this source.

In the process of assessing the cost of capital, the cost of individual elements of equity and debt capital is first assessed, then the weighted average cost of capital is determined.

Determining the cost of capital of an organization is carried out in several stages:

1. identification of the main components that are the sources of formation of the organization’s capital is carried out;

2. the price of each source is calculated separately;

3. the weighted average price of capital is determined based on the share of each component in the total amount of invested capital;

4. measures are being developed to optimize the capital structure and form its target structure.

An important point when determining the cost of capital of an organization

is the choice of the basis on which all calculations should be carried out: before tax or after tax. Since the goal of managing an organization is to maximize net profit, the analysis takes into account the impact of taxes.

It is equally important to determine what price of the source of funds should be taken into account: historical (at the time of attracting the source) or new

(marginal, characterizing the marginal costs of attracting sources of financing). Marginal costs provide a realistic estimate of the organization's future costs required to draw up its investment budget.

The cost of capital depends on its source (owner) and is determined by the capital market, i.e. supply and demand (if demand exceeds supply, then the price is set at a higher level). The cost of capital also depends on the amount of capital raised.

The main factors that influence the cost of capital of an organization are:

· general state of the financial environment, including financial markets;

· commodity market conditions;

· average loan interest rate prevailing in the market;

· availability of various sources of financing for organizations; profitability of the organization's operating activities;

· level of operating leverage;

· level of concentration of equity capital;

· the ratio of the volumes of operating and investment activities; the degree of risk of the operations being carried out;

· industry specific features of the organization’s activities, including the duration of the operating cycle, etc.

The level of cost of capital varies significantly among its individual elements (components). The element of capital in the process of assessing its value is understood as each of its varieties according to individual sources of formation (attraction).

Such elements are capital raised by: 1. reinvestment of the profit received by the organization (retained earnings);

2. issue of preferred shares;

3. issue of common shares;

4 . obtaining a bank loan;

5. bond issues;

6. financial leasing, etc.

For comparable valuation, the value of each element of capital is expressed as an annual interest rate. The level of value of each element of capital is not a constant value and fluctuates significantly over time under the influence of various factors.

Analysis of the structure of the balance sheet liabilities, characterizing the sources of funds, shows that their main types are:

· own sources (authorized capital, equity funds, retained earnings);

· borrowed funds (bank loans (long-term and short-term), bonded loans);

· temporary borrowed funds (accounts payable).

Short-term accounts payable for goods (work, services), wages and taxes are not included in the calculation, since the organization does not pay interest on it and it is a consequence of current operations during the year, while the cost of capital is calculated for the year for making long-term decisions.

Short-term bank loans, as a rule, are temporarily attracted to finance the current needs of production in working capital, so they are also not taken into account when calculating the cost of capital.

Thus, to determine the cost of capital, the most important are its following sources: borrowed funds, which include long-term loans and bond issues; own funds, which include ordinary and preferred shares and retained earnings.

Depending on the duration of existence in this particular form, the organization’s assets, as well as sources of funds, are divided into short-term (current) and long-term. As a rule, it is assumed that current assets are financed from short-term, durable funds, from long-term sources of funds; This optimizes the total cost of raising funds.

Borrowed capital is assessed based on the following elements:

· the cost of a financial loan (bank and leasing);

· cost of capital raised through the issue of bonds;

· the cost of a commodity (commercial) loan (in the form of short-term and long-term deferred payment);

· cost of current settlement obligations.

The main elements of borrowed capital are bank loans and bonds issued by the organization. In some cases, when a significant amount of funds is needed at a time for investment (purchase of new equipment), financial leasing and commercial (commodity) credit (forfetting), loans from other organizations are used.

The cost of borrowed capital depends on many factors: the type of used interest rates(fixed, floating); developed scheme for calculating interest and repaying long-term debt; the need to form a debt repayment fund, etc.

1.3 Dividend policy of an enterprise: concept, specifics and influencing factors

Along with solving investment problems associated with increasing the organization’s assets and determining the sources of their coverage, the process of forming the owner’s share in the profit received in accordance with his contribution, or dividend policy.

Its purpose is to determine the optimal ratio between the consumed and capitalized parts of the profit. In the future, this will ensure the strategic development of the organization, maximize its market value and determine specific measures aimed at increasing the market value of shares.

Dividends- cash payments that a shareholder receives as a result of the distribution of the corporation's net profit in proportion to the number of shares. The broader concept of dividend is used to refer to any direct payment made by a corporation to its shareholders.

The dividend policy of the enterprise includes making decisions on the following issues:

1. Should a business pay out all or part of its net income to shareholders this year or invest it for future growth? This means choosing the ratio of the net profit of the part that goes to pay dividends and the part that is reinvested in the assets of the corporation.

2. Under what conditions should the dividend yield value be changed? Should you stick to one dividend policy over the long term, or can you change it frequently?

3. In what form should the earned net profit be paid to shareholders (in cash in proportion to the shares held, in the form of additional shares or through the repurchase of shares)?

4. What should be the frequency of payments and their absolute value?

5. How to build a policy for paying dividends on incompletely paid shares (in proportion to the paid part or in full)?

· legal restrictions. The purpose of such restrictions is to protect the rights of creditors. In order to limit a company’s ability to “eat up” its capital, the legislation of most countries clearly indicates the sources of dividend policy payments, and also prohibits the payment of dividends in cash if the company is insolvent;

· restrictions due to insufficient liquidity. Dividends can be paid in cash if the company has cash in its current account or cash equivalents in an amount sufficient to pay;

· restrictions due to expansion of production. Enterprises that are at the stage of intensive development are in dire need of sources of financing for their activities. In such a situation, it is advisable to limit the payment of dividends and reinvest profits in production;

· restrictions due to the interests of shareholders. The total income of shareholders consists of the amounts of dividends received and the increase in the market value of shares. When determining the optimal dividend size, it is necessary to assess how the amount of dividends will affect the price of the enterprise as a whole;

In accordance with the Tax Code of the Russian Federation, part I, art. 43, a dividend is any income received by a shareholder (participant) from an organization during the distribution of profits remaining after taxation (including in the form of interest on preferred shares) among shares (stakes) owned by the shareholder (participant).

Decisions on dividend payments of Russian organizations affect both ordinary and preferred shares.

If the level of dividends on ordinary shares depends on the financial results of the organization and is determined by the general meeting of shareholders (on the recommendation of the board of directors), then payments on preferred shares refer to mandatory fixed payments, established in monetary units or as a percentage of the dividend to the par value of the preferred share.

In practice, the following main methods of forming a dividend policy are distinguished:

· conservative;

· compromise, or moderate;

· aggressive.

Each of these methods allows you to develop your own type of dividend policy:

Table 1. Types of dividend policy

Residual dividend policy payments assumes that the dividend payment fund is formed after the need for the formation of its own financial resources, ensuring the full implementation of the company’s investment opportunities, is satisfied through profits.

It is most advisable to implement this policy when the internal rate of return on ongoing projects is higher than the weighted average cost of capital or the level of financial profitability.

IN in this case the use of profits ensures a high rate of capital growth, further development organization and the growth of its financial stability. However, a potentially low level of dividend payments may have a negative impact on the formation of the level of market prices for shares.

Policy of stable dividend payments involves payment of a constant amount over a long period (at high rates of inflation, the amount of dividend payments is adjusted to the inflation index).

The advantage of such a policy is its reliability and the unchanged size of the current shareholder income per share, which leads to stable quotes for these shares on the market. The disadvantage of this policy is its weak connection with the financial performance of the organization.

The policy of a minimum stable amount of dividends with a premium in certain periods has: the advantage that it provides stable guaranteed dividend payments in the minimum stipulated amount with a high connection with the financial results of the organization. This connection allows you to increase the size of dividends during periods of favorable economic conditions without reducing the level of investment activity.

The main disadvantage of this policy is that with long-term payment minimum sizes dividends, the investment attractiveness of the organization’s shares decreases and, accordingly, their market value falls.

Stable dividend rate policy payments provides for the establishment of a long-term rate of such payments in relation to the amount of net profit. The advantage of this policy is the simplicity of its development, and the close connection with the amount of profit generated.

The main disadvantage is the instability of the size of dividend payments per share, determined by the instability of the amount of generated profit. This causes fluctuations in the market value of shares in certain periods and prevents the organization from maximizing the market value of the organization.

Policy of constant increase in dividends provides for a stable increase in the level of dividend payments per share. The increase in dividends occurs, as a rule, in a firmly established percentage increase to their size in the previous period.

The advantage of such a policy is to ensure a high market value of the company's shares and create a positive image among potential investors. The disadvantage is the lack of flexibility in implementing this policy and constant increase financial tension.

The practice of forming a company's dividend policy consists of a number of stages:

First stage - assessment of the main factors determining the formation of dividend policy. In this case, all factors are usually divided into four groups.

1. Factors characterizing the investment opportunities of the organization:

· stage of the company's life cycle;

· the need to expand the company's investment programs;

· degree of readiness of highly effective investment projects for implementation.

2. Factors characterizing the possibilities of generating financial resources from alternative sources:

· adequacy of equity capital reserves, the amount of retained earnings from previous years;

cost of attracting additional

· cost of attracting additional borrowed capital;

Availability of loans in the financial market;

3. Factors associated with objective limitations:

· level of taxation of dividends;

· level of taxation of property of organizations;

· achieved effect financial leverage;

· the actual amount of profit received and the level of return on equity.

4. Other factors:

· the market cycle of the product market in which the company is a participant;

· level of dividend payments by competing companies;

· urgency of payments on previously received loans;

· the possibility of losing control over the management of the company;

IN second stage - choosing the type of policy that would correspond to the company's strategy;

T third stage - determination of the profit distribution mechanism corresponding to the company's strategy.

The organization’s dividend policy takes into account the entire range of interests: obtaining additional resources for investment through the issue of shares, ensuring a sufficient dividend to their holders, optimizing the “profit - investment - dividend” ratio, taking into account real conditions development of the organization.

The dividend policy intertwines the interests of the company as a whole and the interests of shareholders. Effectively connecting these interests is one of the important tasks of the company's financial strategy.

2. Mmethods and models of financial planning

Financial planning- intra-company planning subsystem. Objects of financial planning:

1 . financial resources are monetary income and receipts at the disposal of a commercial organization and intended for the implementation of expenses for expanded reproduction, economic stimulation, fulfillment of obligations to the state, and financing of other expenses;

2 . financial relations - monetary relations arising in the process of expanded reproduction;

3 . cost proportions - proportions that are formed during the distribution of financial resources. These proportions must be economically justified, since they affect the efficiency of a commercial organization;

4 . financial plan of an enterprise is a document reflecting the volume of receipts and expenditures of funds, fixing the balance of income and areas of expenditure of the enterprise, including payments to the budget for the planned period.

Goals financial planning of a commercial organization depends on the selected criteria for making financial decisions, which include maximizing sales; profit maximization; maximizing the property of company owners, etc.

Main goals financial planning - providing financial resources for production, investment, and financial activities of an enterprise; determining ways to effectively invest capital, assessing the degree of its rational use; identification of internal reserves for increasing profits; establishing rational financial relations with the budget, banks, counterparties; respecting the interests of investors; control over the financial condition of the enterprise.

The importance of financial planning lies in the fact that it embodies the developed strategic goals in the form of specific financial indicators; provides financial resources for the economic development proportions laid down in the production plan; provides an opportunity to determine the viability (effectiveness) of an enterprise project in a competitive environment; serves as the basis for assessing investment attractiveness for investors.

Financial planning at an enterprise includes three main subsystems: long-term financial planning, current financial planning, operational financial planning.

Strategic financial planning determines the most important indicators, proportions and rates of expanded reproduction, and is the main form of realizing the goals of the enterprise. Covers a period of 3-5 years. Period from 1 year to 3 years wears conditional character, since it depends on economic stability and the ability to predict the volume of financial resources and directions of their use. As part of strategic planning, long-term development guidelines and goals of the enterprise, a long-term course of action to achieve the goal and allocate resources are determined. Search is underway alternative options, the best is selected, and the enterprise strategy is based on it.

Long-term financial planning is "implementation" planning. Covers a period of 1-2 years. Based on the developed financial strategy and financial policy for individual aspects of financial activity. This type of financial planning consists in developing specific types of current financial plans that enable the enterprise to determine for the coming period all sources of financing its development, form the structure of its income and costs, ensure its constant solvency, and also determine the structure of its assets and capital of the enterprise at the end planned period.

The result of current financial planning is the development of three main documents: a cash flow plan; profit and loss statement plan; balance sheet plan.

The main purpose of constructing these documents is to assess the financial position of the enterprise at the end of the planning period. The current financial plan is drawn up for a period of 1 year. This is explained by the fact that within 1 year, seasonal fluctuations in market conditions generally level out. The annual financial plan is broken down quarterly or monthly, since the need for funds may change during the year and in some quarter (month) there may be a lack of financial resources.

Short-term (operational) financial planning complements long-term; it is necessary in order to control the receipt of actual revenue into the current account and the expenditure of available financial resources. Financial planning includes drawing up and executing a payment calendar, cash plan and calculating the need for a short-term loan.

Conclusion

Long-term financial policy should be aimed at implementing structural changes, accelerating scientific and technological progress, and reorienting social production to meet social needs and improve the living standards of the population.

In general, it seems promising to carry out budget expenditures based on optimizing their volume and structure to the extent of increasing income based on increasing the efficiency of material production, the basis for which is created by new economic levers of management, development and strengthening of full self-financing and self-financing at all levels of management.

One of the basic principles of long-term financial policy is that it should be based not so much on the actual situation as on the forecast of its changes. Only on the basis of foresight does financial policy become sustainable. This aspect is modern conditions the financial crisis is the most pressing.

List of used literature